es

AENA SME, SA

67

Airports

4

Countries

69

Reports

Login/Register

© Pascal Meier / Unsplash

es

Airports

Countries

Reports

tr

Airports

Countries

Reports

In the post-COVID era there has been plenty of speculation on the role that the private sector, and public-private partnerships (PPPs) in particular, might play in airport ownership and development.

Several governments had to give financial support to airports during the past two years when their gateways had little to no business and this has acted as a wake-up call. Is it justified that taxpayer dollars are spent on bailing out airports during a crisis when private sector-owned airports would ordinarily go to the debt markets to see them through a rough patch?

Of course, COVID19 was more than a rough patch, which is why there was even more discussion on the way forward for future airport operations and financing. In the US alone—where airport public-private partnerships are rare—lawmakers allocated about $10 billion in economic relief to eligible American airports via the March 2020 CARES Act (which made available $2.2 trillion in total across many sectors).

The funds for airports were distributed by the Federal Aviation Administration (FAA) through the Airport Coronavirus Response Grant Program (ACRGP). Most of it was shared between commercial service airports; those with more than 10,000 annual passenger boardings. Including concession relief, the amount of public money handed out was substantial, covering a large number of gateways.

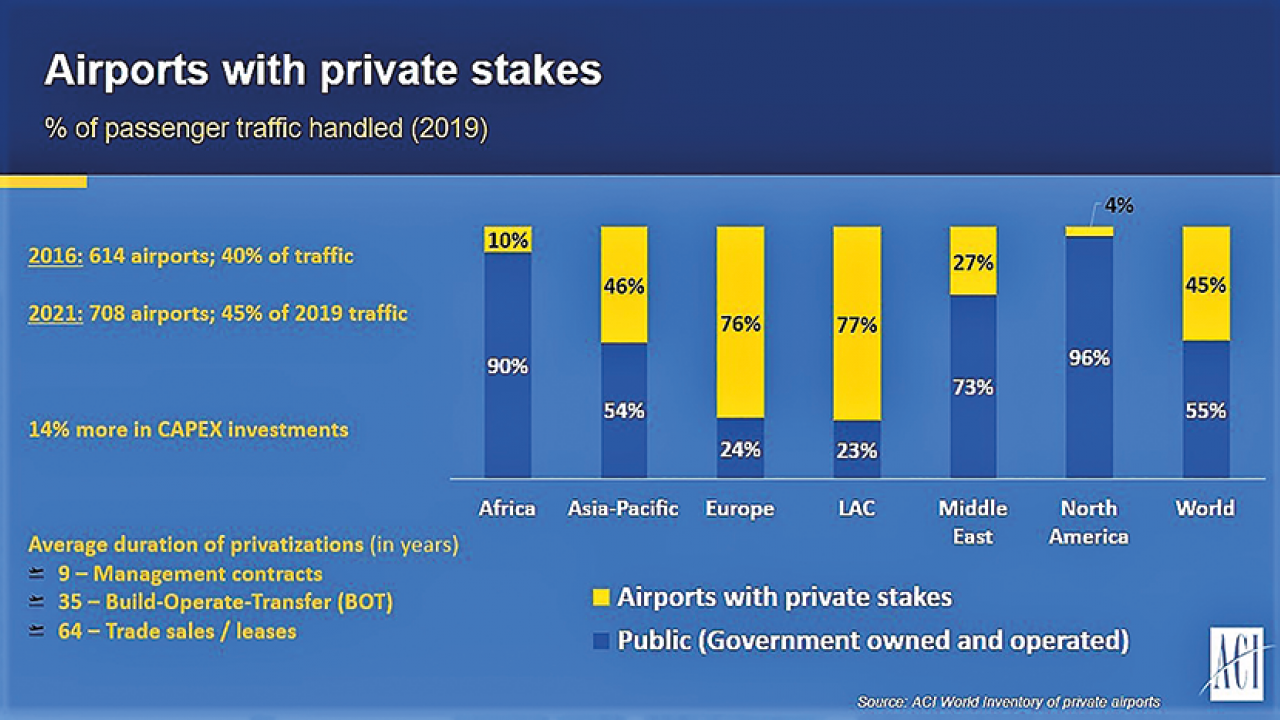

The US and Canada are a special case because here private sector participation in airports is tiny at just 4% based on passengers handled in 2019 as most gateways are owned by local municipalities (see chart below). The only other region that has such low private sector participation is Africa at 10%, but that is gradually changing. By contrast, the share in Europe and South America is 76% and 77% respectively, with a global average of 45%, according to ACI data.

Levels of privatization vary by region.

© ACI World

Amid these regional variations, what is in no doubt is that private sector participation is growing. In 2016, there were 614 airports with private stakes and they processed 40% of all passengers. Within a few years that number had risen to 708 airports handling 45% of passengers (based on 2019 traffic).

Admittedly, there are some arguments why American-style state funding and operation of airports can be a good thing during hard times. After years of almost non-stop annual passenger growth, COVID19 ensured that—for the first time in decades—traffic risk has become a talking point.

Airport capital expenditure (CAPEX) contracted in 2020 and 2021 relative to 2019 “in the realm of double digits during the worst days of the pandemic”, according to ACI World’s vice president and chief economist, Patrick Lucas.

Markets with more privatized airports, like Europe and Latin America, suffered some big setbacks as capital spending was reduced due to financial shortfalls.

On the other hand, markets like the US—thanks to the CARES Act and institutionalized federal subsidies pumped into airport infrastructure—saw less of an impact on CAPEX investment. Asian and African markets meanwhile were a bit more varied in their spending deferment.

In the good times, however, private sector involvement is often encouraged. Private operators are usually very willing—and faster—to invest if they can see that the returns will be good. Right now, in a strong recovery phase for aviation, investors are more likely to see the positives across 5+ year horizons.

The latest (seventh) round of airport privatizations in Brazil, where the highest bid from AENA was more than three times the asking price, is evidence of this trend. Through AirportIR.com, Modalis closely tracks active and potential upcoming deals in the global markets and we are seeing an uptick in activity now that the worst of COVID seems to be behind us.

Earlier this year, ACI World’s Lucas explained in a podcast from the World Association of PPP Units & Professionals (WAPPP) that a fundamental evolution had taken place in the airport-airline relationship and that more risk-sharing would be the future. He said: “If we have learned anything from the pandemic, we know that we have to share risks a bit better.” Not just to recover losses from the pandemic but to ensure a more stable financial environment during future crises.

As part of this redrawing of the risk map, ACI expects to see more renegotiations of agreements in the non-aeronautical business, especially when it comes to dealing with uncertain traffic volumes. For example, this is true of minimum annual guarantee (MAG) contracts, and the increasing use of joint ventures, one of the latest being between India’s Bengaluru Airport and travel retailer Dufry, where the airport landlord and their concessionaire work in closer partnership.

At the macro level of airport terminals and whole airports, many smaller or financially-constrained governments have found it easier, and more cost-effective, to hand over airport operations via PPPs that act as a national revenue generator.

The impetus is evident in many parts of the Caribbean and increasingly in South America. Africa is also getting renewed interest, with TAV Airports, for example, aiming to expand its footprint on the continent via Lagos, Nigeria, on the back of high traffic expectations.

In the US, too, the PPP bug has selectively taken hold. At New York’s LaGuardia and JFK International airports the landlord, the Port Authority of New York and New Jersey, has been active in pushing ahead with PPP deals with an impressive outcome at LGA Terminal B. The latest $4.2 billion deal for Terminal 6 was closed in November 2022 with JFK Millennium Partners.

Terminal transformations from ugly ducklings to beautiful swans—if they continue to go well—will almost certainly be seen as an example to other US states wanting to improve their passenger experience. A collaborative process that requires less from the public purse but produces good—or even better—outcomes for users is hard to ignore.

[Part 2 of this article will be published on Wednesday, February 8th.]