Login/Register

Ryanair Throttles Back in Spain: Which Rivals Will Step in?

Dion Zumbrink

October 22, 2025

The sun is setting on certain Ryanair routes in Spain.

© Piotr Mitelski /

Ryanair is trimming its Spanish capacity, first with an estimated 10% winter cut (representing some one million seats) concentrated at regional airports and the Canary Islands, followed by an additional 1.2 million seats in summer 2026. This will include a total exit from Asturias in Northwest Spain.

The moves led to a very public dispute with airport operator Aena over fee increases. With that as the backdrop, it is worth looking at Ryanair’s position in Spain and what happens with the gap left behind.

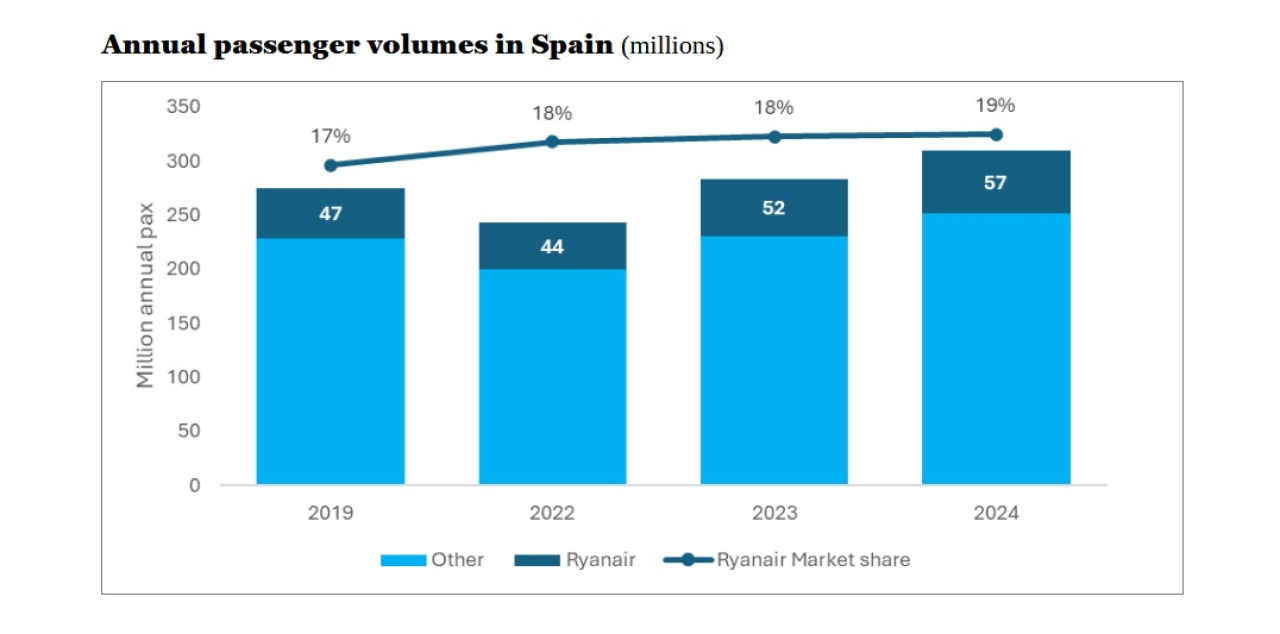

By the end of the last decade, Ryanair had become Spain’s largest airline, transporting just under 50 million passengers in 2019 (see chart below). The airline balanced holiday routes with an extensive domestic network and year-round city-pair connections.

© Dion Zumbrink

Ryanair’s Powerful Position Post COVID

The post-pandemic rebound then strongly boosted growth as leisure demand surged and Spanish airports recovered faster than many low-cost carrier (LCC) peers. Ryanair transported an impressive 23% more passengers in Spain in 2024 than in 2019.

Even with the cuts, Ryanair’s market lead is so comfortable that it will remain Spain’s largest airline. Over the full year 2025, it will account for around 19% of all capacity to, from, and within Spain (around 22% in summer high season), ahead of IAG’s Vueling and Iberia, operating from 25 Spanish airports on over 750 routes.

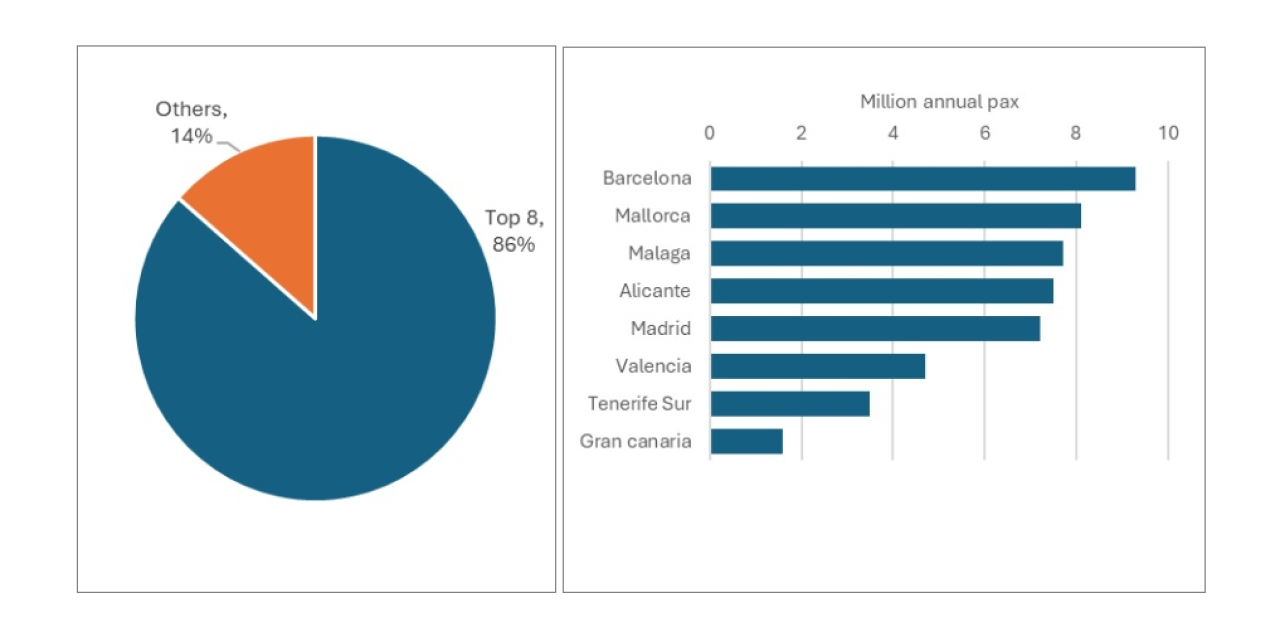

Some 86% of Ryanair´s traffic (around 50 million passengers) is concentrated in the eight largest airports in the country, with the remaining seven million is distributed across regional airports (see the two charts below).

© Dion Zumbrink

Ryanair is mainly cutting capacity at those smaller gateways, while at Málaga, for example, capacity will grow by 7% in the upcoming winter season. Therefore, near-term pain will be concentrated at locations where Ryanair has been the primary stimulator of demand. Some capacity will be backfilled by competitors, but shoulder-season frequencies and thinner point-to-point links are most vulnerable.

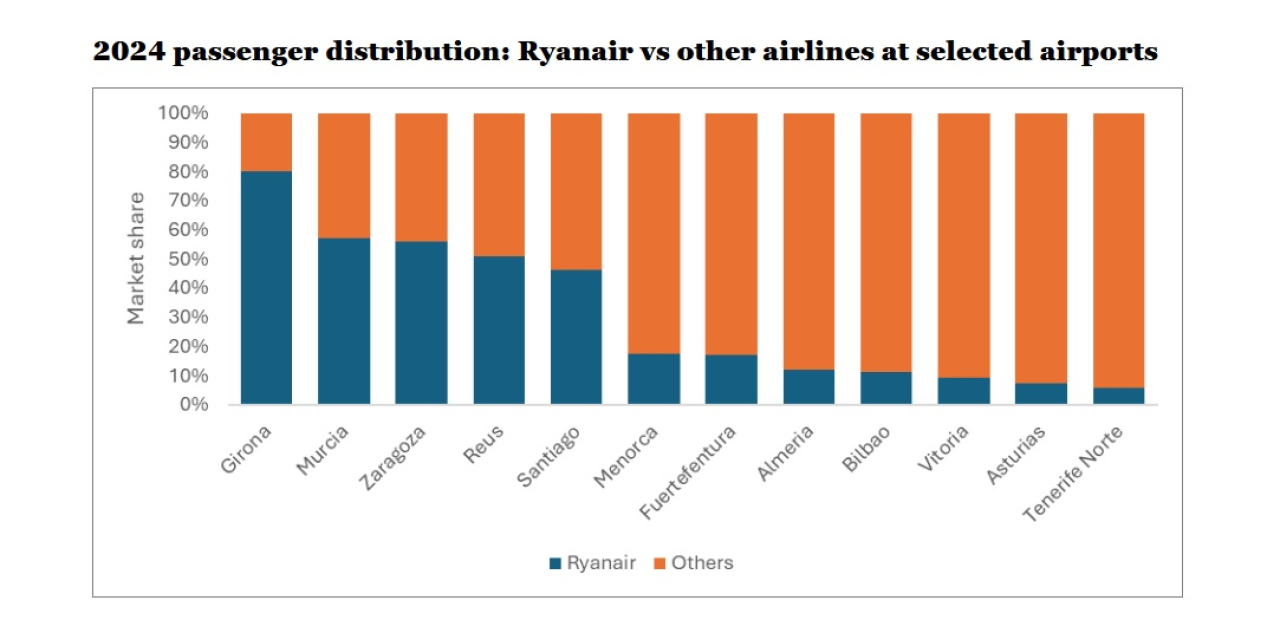

Looking at the smaller airports where Ryanair is active, it can be seen that Girona is especially under threat (see chart below). Another four gateways—Murcia, Zaragoza, Reus, and Santiago—where the airline holds around 50% of the market, are also highly compromised. At the rest of the airports, however, Ryanair’s share is significantly lower, and a capacity reduction would be far less impactful.

© Dion Zumbrink

Who Will Fill the Gaps?

Several airlines can jump in, but the near-term picture is different by segment, with domestic and island markets easiest to repair, while thinner regional links are most exposed. The options are:

-

Vueling, Spain’s second-largest airline, which has already indicated it will expand in Santiago and Tenerife Norte

-

Iberia Express, which moved first in the Canaries, adding around 30,000 winter seats and 116 flights, with roughly half of the extra capacity located at Tenerife Norte, one of the airports hit by Ryanair’s cuts

-

easyJet, the most natural LCC substitute on UK–Spain routes and other northern European sun markets, with the brand and aircraft basing already growing fast in Málaga, Alicante, Palma, and the Canaries. However, no specific expansion intentions have been published to date.

-

Volotea, whose bread-and-butter is secondary city-pairs. The airline has scaled up in Asturias and is well placed to fill certain specific year-round domestic demand that Ryanair drops.

-

Wizz Air, which is expanding in Spain with about 10 million seats offered in total from Spain in 2025, and more routes coming in 2026. This positions the LCC to take some of Ryanair’s regional airport space. However, it remains to be seen if the airline will opt for smaller markets.

With underlying demand drivers for tourism still strong, the overall airline offer to the key Spanish tourism regions is not at risk, as there are sufficient players eager to enter the market. At the regional level, the impact will likely only be of significance at a handful of airports where Ryanair operates more than 40% of traffic.