Login/Register

European Aviation Flows Vividly Redrawn by Middle-East Conflict

Dion Zumbrink

June 24, 2026

An Emirates A380 near Concourse A at DXB.

© Emirates

European aviation continued to grow in the first five months of 2026, but the regional picture has become increasingly uneven, with the Middle East in heavy decline, according to data from pan-European organization Eurocontrol.

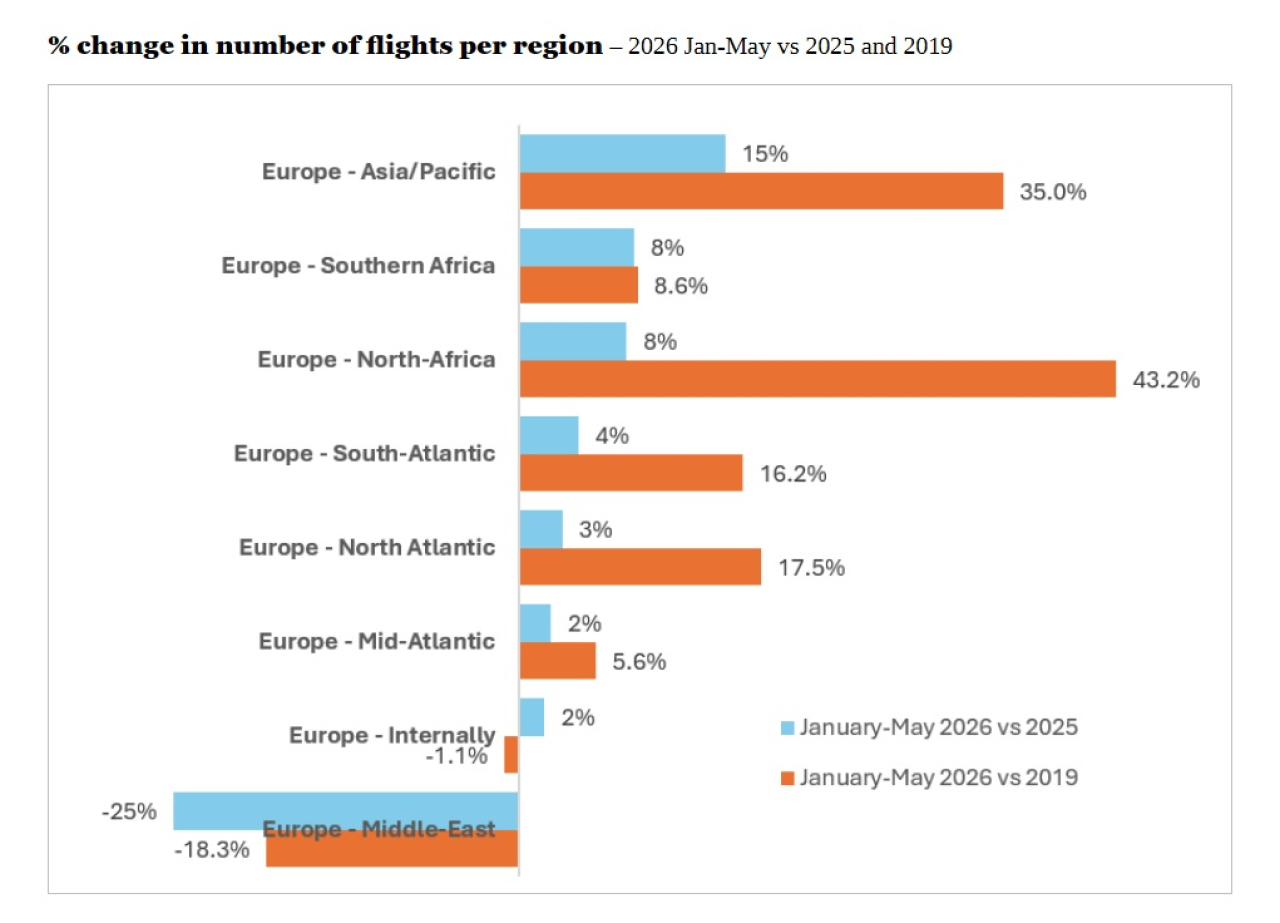

Most external European flows from January to May 2026 remained above both 2025 and 2019 levels to varying degrees. Europe–Asia/Pacific flights increased by 15% compared to the same period in 2025 and are now 35% above 2019. Europe–North Africa is also very strong, with 8% growth versus 2025 and 43.2% growth versus 2019.

Internal European flights were relatively flat compared to 2019, but this headline masks large differences between individual country-pair markets and airports. Several major domestic markets declined, including Germany, France, and the UK. At the same time, other flows, mainly between northern and southern Europe, increased significantly.

Europe–Middle East Impact From the Conflict

The clear exception is the Europe–Middle East flow. Flights on this corridor declined by 25% compared to 2025. This decline is the clearest impact of the US-Iran conflict on European aviation flows (see chart below).

Adapted from data supplied by Eurocontrol.

© Dion Zumbrink/Eurocontrol

Major Middle East hub airlines are still only operating an average of 70-85% of daily flights compared to pre-war, although these carriers are now ramping up capacity to normal levels. Etihad, for example, indicated that it expected to be flying above its previous year’s level by mid-June. Emirates also stated that it did not intend to reduce capacity and will use incentives to win back passengers. This suggests that the large Gulf carriers are trying to protect their network position despite higher costs.

Many non-Gulf airlines, however, are more cautious. Several European carriers continue to avoid parts of the region or have extended suspensions to destinations such as Dubai, Baghdad, Erbil, Tel Aviv, Beirut, and other Middle Eastern airports.

The current status as of June 2026 is therefore mixed. The immediate shock has partly eased, and the major Gulf carriers are restoring capacity. But the traffic flow has not fully normalized and has significantly reshaped patterns for European air travel.

Asia/Pacific Growth Remains Strong

The most interesting countertrend is the high growth in Europe–Asia/Pacific flights. Despite the Middle East disruption, this flow increased by 15% versus 2025 and is 35% above 2019. This shows that demand between Europe and Asia remains strong, but also that the market has partly adjusted around the disruption.

Several factors explain this. First, Asia-Europe travel was still recovering and expanding after the pandemic. Second, some airlines have maintained or increased direct services between Europe and Asia, particularly where demand and yields are solid. Third, some 20% of Europe-Asia passengers transit through the Gulf, and part of the traffic may now be routed on direct services. This was evidenced by, for example, Singapore Airlines reporting a surge in load factors from a typical 80% to over 93% on their Europe flights.

Many airlines still face longer flight times and higher costs/air fares because Russian and Middle Eastern airspace limitations reduce routing options. Therefore, the strong Asia/Pacific growth can be seen as evidence of very resilient structural demand.

North Africa is the Fastest-growing Market

Europe–North Africa has one of the strongest-growing flows in the chart above. Flights are up 8% versus 2025 and 43.2% above 2019. This continues a trend already visible in recent years, with strong growth to Morocco, Egypt, Tunisia, and Algeria.

This market benefits from several structural factors. It is close to Europe, relatively fuel-efficient to serve, and strongly linked to leisure, VFR, and diaspora travel. Moreover, low-cost carriers and tour operators have expanded capacity to North African destinations. In a period when longer-haul flying is more expensive and geopolitically exposed, nearby leisure markets become more attractive for airlines. This is very much in line with the growth of the Southern European destinations.

All of this results in a change in European aviation flows. Middle East traffic is not disappearing, but it is being redistributed. More growth is visible on direct Asia routes, North Africa, Southern Europe, and the North Atlantic, while the Middle East corridor is being impacted by the ongoing conflict. This is the result of leisure passengers opting for closer-by, cost-efficient and safer destinations, while resilient demand on the Asia corridor is making the most of direct connections.