Login/Register

Impressive Growth for KSA, in Pursuit of a Lofty 330m Traffic Target

Dion Zumbrink

February 25, 2026

Foster + Partners' design for the new King Salman International Airport.

© Foster + Partners

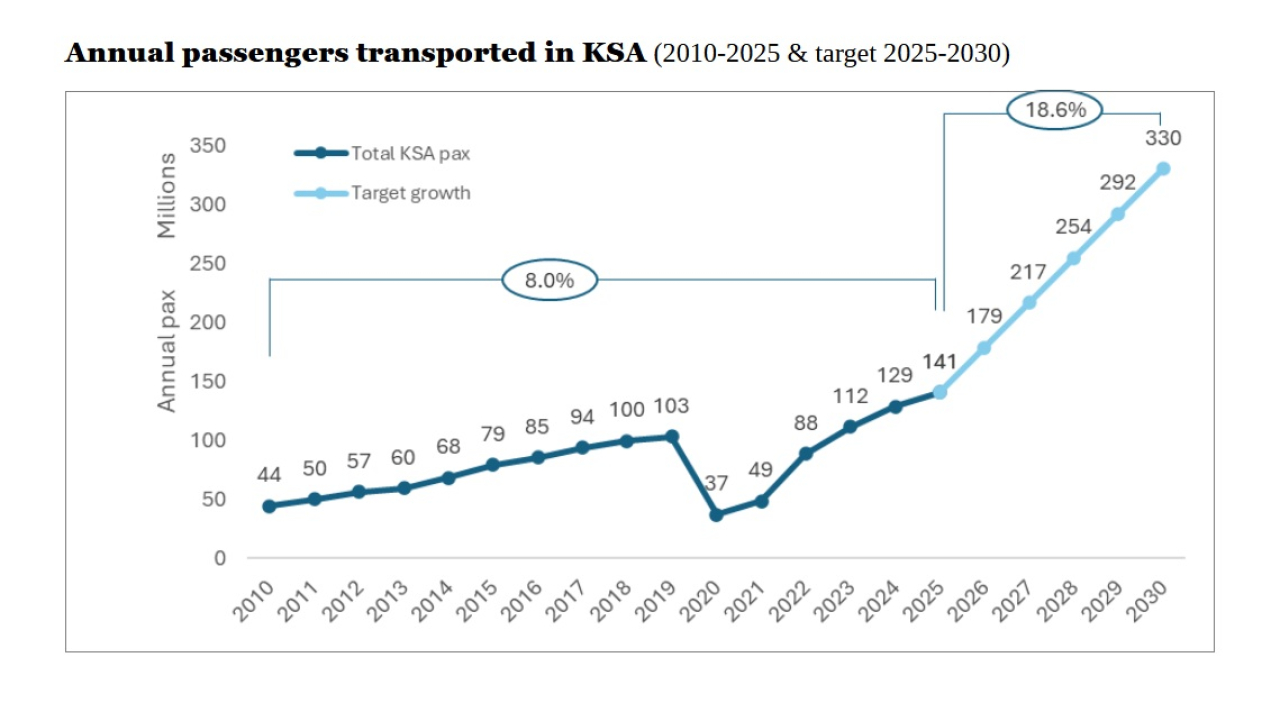

Saudi Arabia has put a hard number on its aviation ambition for the end of this decade: 330 million passengers annually by 2030, alongside connectivity to 250+ destinations. The target is embedded in the kingdom’s 2022 Saudi Aviation Strategy. However, since then, the fall in the oil price and subsequent recent scaling back of mega projects may directly impact the realization of this target.

KSA has posted rapid and sustained growth post-pandemic, achieving 9.6% growth in 2025 to reach 141 million passengers. This is 36% over the 103 million passengers carried in 2019. But the target of 330 million passengers by 2030 is demanding; it implies a compound annual growth rate (CAGR) of over 18% over five years (see chart below).

Planned growth between 2025 and 2030 is steeper than that seen up to 2025.

© Dion Zumbrink

There are ambitious projects underway that could support this target if all plays out as envisioned. These would benefit aviation growth in smaller, regional airports that are planned for, or currently undergoing, privatization. Abha International Airport, Qassim Airport, Taif Airport, and Hail Airport are keylocations in the airport privatization pipeline, with Abha already in procurement.

The key enablers of growth beyond past track record and organic demand are capacity-based. For example, Riyadh’s King Salman International Airport (KSIA), still in development, is expected to be the single biggest physical enabler. The planned mega-hub will expand the footprint of King Khalid Airport (RUH). Official project communications state a goal of up to 120 million passengers annually for KSIA by 2030.

Saudi Arabia’s 330 million target is not feasible without at least one true global connecting hub at the scale of Gulf mega-hubs. KSIA is explicitly positioned to do that through an enlarged network and frequencies. This will also benefit the domestic network via connections to smaller airports. Delivery has moved from planning to execution, with reports suggesting that work began in December 2025 with the construction of a third runway.

Tourism Projects Under Review

Jeddah’s King Abdulaziz International Airport (JED) is already operating at scale, recording 53.4 million passengers in 2025. Jeddah is tied to Hajj/Umrah and Red Sea tourism growth, so expansions and operational upgrades here translate directly into passenger throughput (especially seasonal peaks). Significant tourism projects support this potential, although recent scale-backs risk JED’s future traffic goals.

Landscaped gardens and multiple buildings will strongly feature in the design of the new Abha Airport.

© Foster + Partners

Tourism is a core pillar underpinning Saudi Arabia’s aviation growth, with the kingdom targeting 150 million annual visitors by 2030 across religious, leisure, cultural, and business segments. To stimulate inbound travel, Saudi Arabia has rolled out large-scale destination development (Red Sea, AlUla, Diriyah, and NEOM), several global events spanning sports, entertainment, and culture, and a liberalized visa system through e-visas and visa-on-arrival for many markets.

New airports will also enable direct access to key destinations: NEOM’s planned airport is set to provide 25 million capacity, while Red Sea International Airport (RSI) is targeting one million passengers per year by 2030. Other existing airports, such as the Qassim and Al Ula gateways, are also expected to receive a boost in tourism.

Airline Capacity Another Factor

Fundamental to the traffic growth is the expanded seat supply by KSA’s airlines. Riyadh Air was created to help build a KSIA-based global network, with some 120 aircraft on order (60 A321neos, 64 A350s and B787s). The airline launched cargo operations in January, and passenger aircraft deliveries are expected to commence at the end of 2026 for narrowbodies and 2027 for widebodies.

Low-cost growth continues with flynas publicly framing an expansion to 160 aircraft by 2030 with a much larger destination and route map. Meanwhile, Saudia Group’s flyadeal plans close to 100 aircraft by 2030 and is moving into longer-haul flying with A330neo deliveries from 2027 to open new leisure/VFR markets.

Saudi Arabia is clearly on track for strong growth—the jump from 128 million (2024) to 141 million (2025) demonstrates continued success in the execution of its strategy. However, 330 million by 2030 is still a stretch, and is based on capacity enhancement rather than organic demand growth. It is achievable only if KSIA ramps up construction and operational readiness on time, Riyadh Air scales quickly into a true connecting carrier, and key tourism mega-projects develop according to plan.