Login/Register

African Aviation Momentum is Building

Dion Zumbrink

November 19, 2025

© James Wiseman / Unsplash

Africa’s aviation potential has been heralded for years due to its strong demographic, geographic, and economic fundamentals. However, to date, the continent has struggled to convert this potential into sustained growth.

The rapidly growing population and middle-class, untapped tourism markets, distances between major cities, and the promise of the African Continental Free Trade Area (AfCFTA) and Single African Air Transport Market (SAATM) all make this a real possibility. The main question is, when can it be expected?

African Aviation Makes Progress in 2025

There are, finally, clear signs that momentum is coming. The African Union’s recent US $30 billion aviation infrastructure investment commitment reflects a growing political awareness that aviation is crucial for Africa’s economic development.

Simultaneously, the number of new airport developments, private-sector partnerships and national airline expansions is gathering pace. With some high-profile hub airport projects active in 2025, Africa’s long-anticipated aviation growth may finally become a reality. Examples of planned expansion projects include Addis Ababa (greenfield 100 MPax capacity), Kigali (greenfield 14 MPax capacity), Casablanca (expansion to 35 MPax capacity), Luanda (greenfield 15 MPax capacity), and Nairobi (expansion to 20 MPax capacity).

It seems that currently there is a confluence of political attention, significant investment, and a growing project pipeline, which suggests that momentum is building in ways that were previously hoped for but not realised. So, which countries and investors will seize the opportunity?

Africa Market Overview

While the ongoing efforts will only drive growth in the medium-term, the 2025 performance confirms the path taken is the right one. ACI’s latest World Airport Traffic Report is forecasting Africa to be the fastest growing region this year, up 9.4% and transporting 273 million passengers.

Africa's growth will outstrip other regions this year.

© Dion Zumbrink

Several key indicators suggest that the aviation industry is only at a starting point. For example, the continent still has only 20% low-cost carrier (LCC) capacity, compared to 35% in Europe, Latin America, and North America, and up to 52% in Southeast Asia. One or more strong intra-regional LCCs are fundamental to drive air traffic and unlock access to an ever-growing middle-class segment on the continent.

Africa's LCC share is shown here in orange.

© Dion Zumbrink

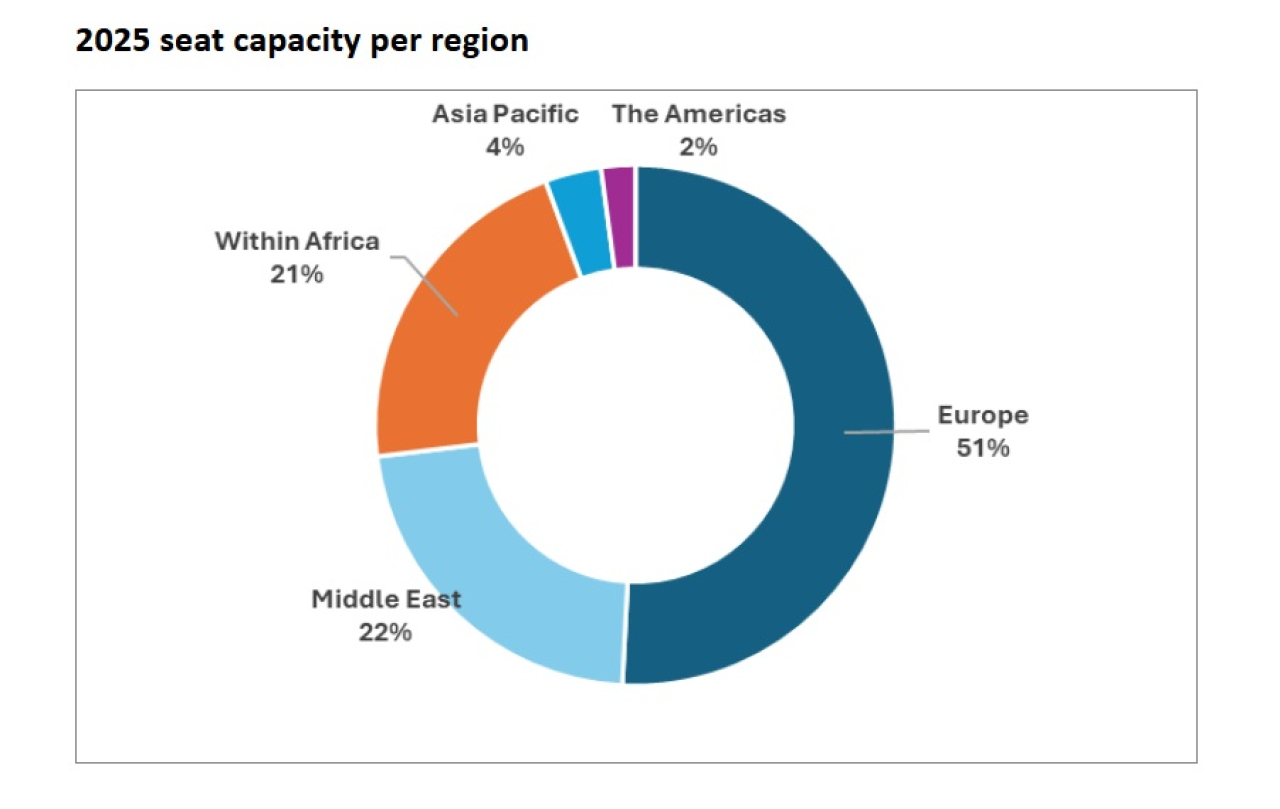

Furthermore, it is remarkable that only 21% of total seat capacity is within Africa, while the distances between major cities are large, and often no reasonable alternative travel mode is available. This shows that the internal market is far underdeveloped, often due to a lack of airport infrastructure, airline capacity, and inefficient bilateral agreements. Typically, a well-developed internal market would make up more than half of traffic.

Europe dominates seat capacities to Africa.

© Dion Zumbrink

Europe is the largest partner to Africa, but mainly to North African tourism destinations along the Mediterranean Sea and the Red Sea. Asia only accounts for 4% of all seats from the continent, although the Middle East, which has a significant 22% share, is thought to service some Asian demand as it offers good connections to the continent.

Next Steps Required

The airport and airline developments currently in motion will help drive the internal market, thus better connecting key economic centres in Africa. Thereafter, they will drive the overall development of the continent in the upcoming decades.

Next, the continent needs a strong LCC, such as Air Arabia or FlyDubai or a European player. There are, however, structural challenges that are more complex than in Europe or the Middle East, which need to be resolved.

The single biggest constraint to LCC development in Africa is market access. Full implementation of SAATM, or at least bilateral smaller-scale SAATMs between clusters of countries, is essential. Without liberalisation, an LCC cannot build the wide, dense network needed to gain economies of scale. In addition, all new airport projects need to consider facilities for LCCs, i.e. low-cost terminals, aprons with fast turnaround times and no airbridges, plus amended airport charges.

While major progress is being made, a true SAATM and the rise of a regional LCC are now the next major steps that must be taken to realise the evident potential of the African market.