Login/Register

North America is the Only Region to Return to Profitability in 2022, but Passenger Forecasts Cut

Kevin Rozario

December 7, 2022

© Heathrow Airport Limited

Airline finances are improving faster than expected. International Air Transport Association (IATA) data suggest that financial performances continue to improve since the depth of the pandemic losses seen in 2020, but that North America—chiefly the United States—will be the only region to return to profitability this year.

In 2023, two other regions will join ranks with North America: Europe and the Middle East, while Latin America, Africa, and Asia-Pacific will remain in the red.

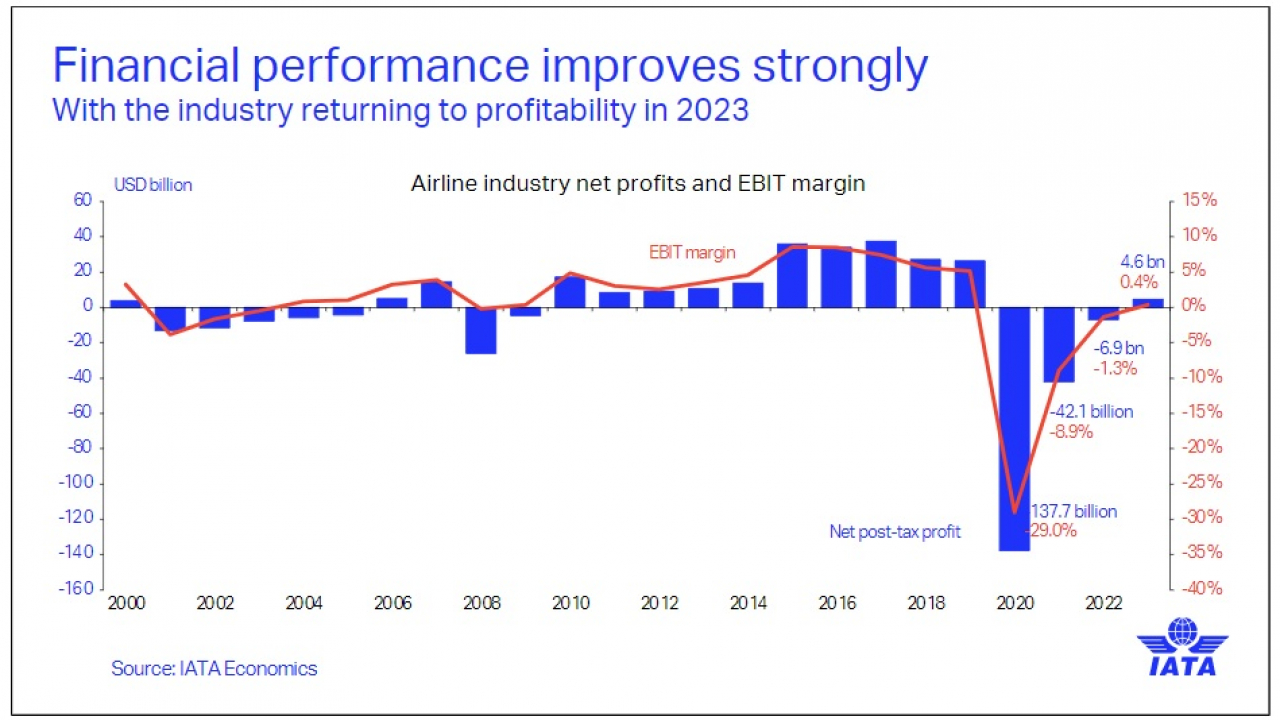

Overall, IATA expects a return to profitability for the global airline industry in 2023, posting a small net profit of $4.7 billion—a 0.6% net profit margin. It is the first profit since 2019 when industry net profits were better at $26.4 billion with a much healthier net profit margin of 3.1%.

For this year, airline net losses are expected to be $6.9 billion which is an improvement on the $9.7 billion loss IATA had forecast in June. In 2021 and 2020 losses were $42 billion and $138 billion respectively, so the rebound in 2022 is significant.

Airlines have cut costs to become profitable quickly.

$800 Billion in Revenue Just to Turn a Small Profit

Referencing the return to profit next year, IATA’s Director General, Willie Walsh, commented: “That is a great achievement considering the scale of the financial and economic damage caused by government-imposed pandemic restrictions. But a $4.7 billion profit on industry revenues of $779 billion also illustrates that there is much more ground to cover to put the global industry on a solid financial footing.

He added: “Many airlines are sufficiently profitable to attract the capital needed to drive the industry forward as it decarbonizes. But many others are struggling for a variety of reasons. These include onerous regulation, high costs, inconsistent government policies, inefficient infrastructure, and a value chain where the rewards of connecting the world are not equitably distributed.”

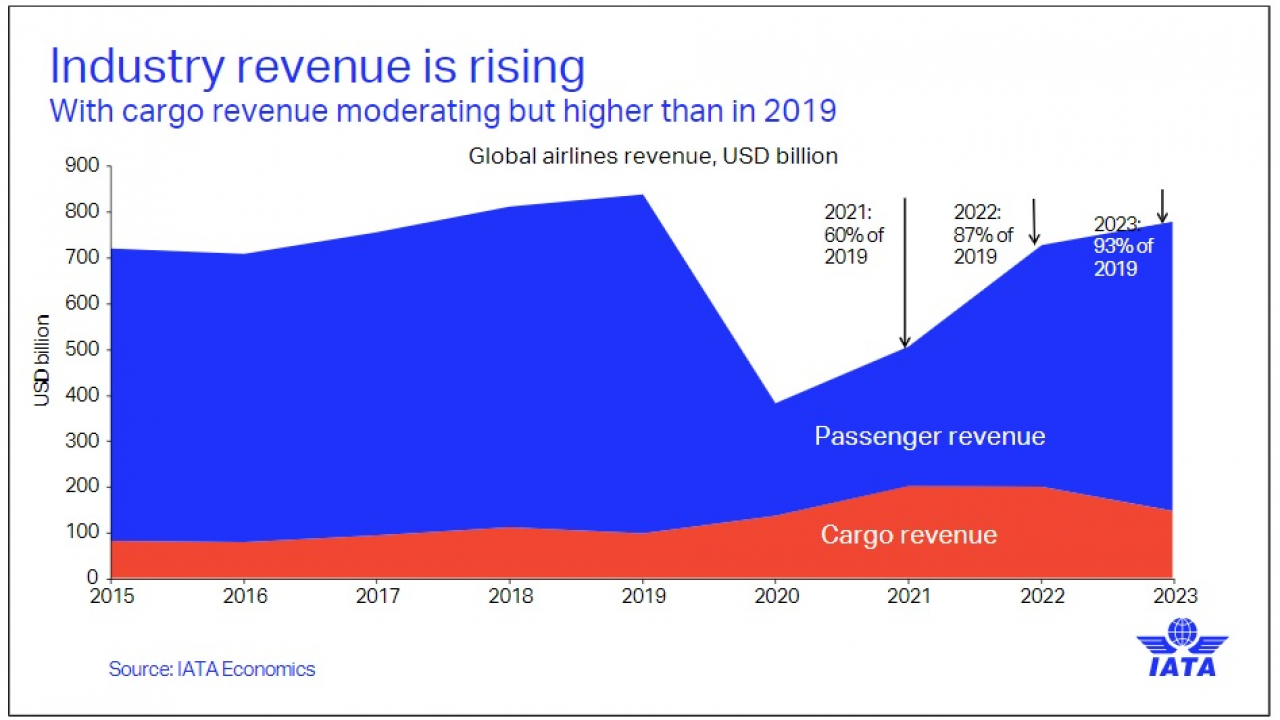

The improved financial position this year is largely thanks to strengthened yields and strong cost controls in the face of rising fuel prices. Passenger yields are expected to grow by 8.4% (up from 5.6% anticipated in June). Passenger revenue is expected to reach $438 billion (up from $239 billion in 2021). Air cargo has also played a crucial role in cutting losses with revenues expected to top $200 billion. That is more than double the $101 billion earned in 2019.

The split between passenger and cargo revenue moved very much in cargo’s favor during the pandemic.

Not All Good News

China remains a drag on the airline market where delays in removing COVID19 restrictions are hampering progress, though some easing has now begun. Also, while profitability has been better than expected, numbers have not. IATA’s June forecast anticipated that passenger traffic would reach 82% of pre-crisis levels this year, but it now appears that demand will only reach 71% of pre-crisis levels.

On the cost side, jet kerosene prices are expected to average $138.8/barrel for the year, much higher than the $125.5/barrel expected in June. That reflects higher oil prices and inflates the industry’s fuel bill to $222 billion, well above the $192 billion anticipated in June.

“With some key markets like China retaining restrictions longer than anticipated, passenger numbers fell somewhat short of expectation. We’ll end the year at about 70% of 2019 passenger volumes. But with yield improvement in both cargo and passenger businesses, airlines will reach the cusp of profitability,” said Walsh.