Login/Register

Why United States-Mexico Air Traffic is on a Growth Path (Part 1)

Dion Zumbrink

May 17, 2023

© Andrew Schultz / Unsplash

Mexico is, by far, the largest country for U.S. international air travel following the pandemic. It has dethroned Canada which, historically, has been the top foreign air traffic destination. The southern U.S. neighbor is now, in fact, the largest international air travel country pair in the world.

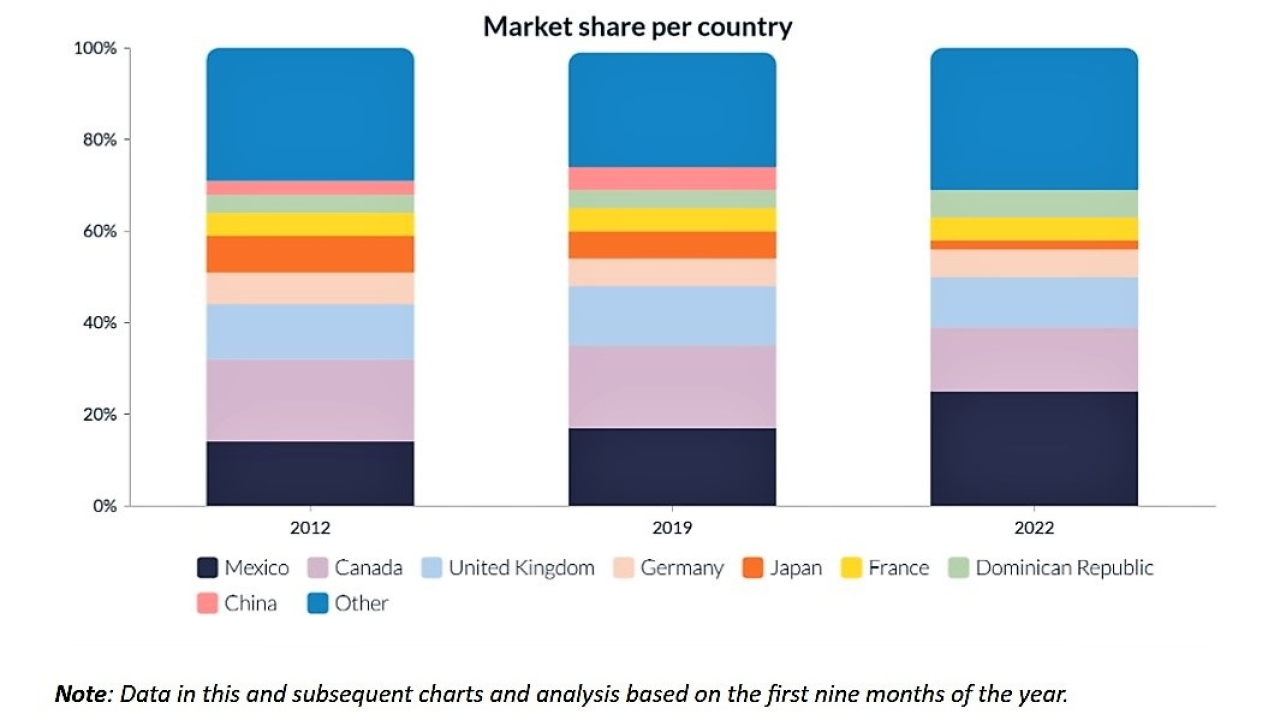

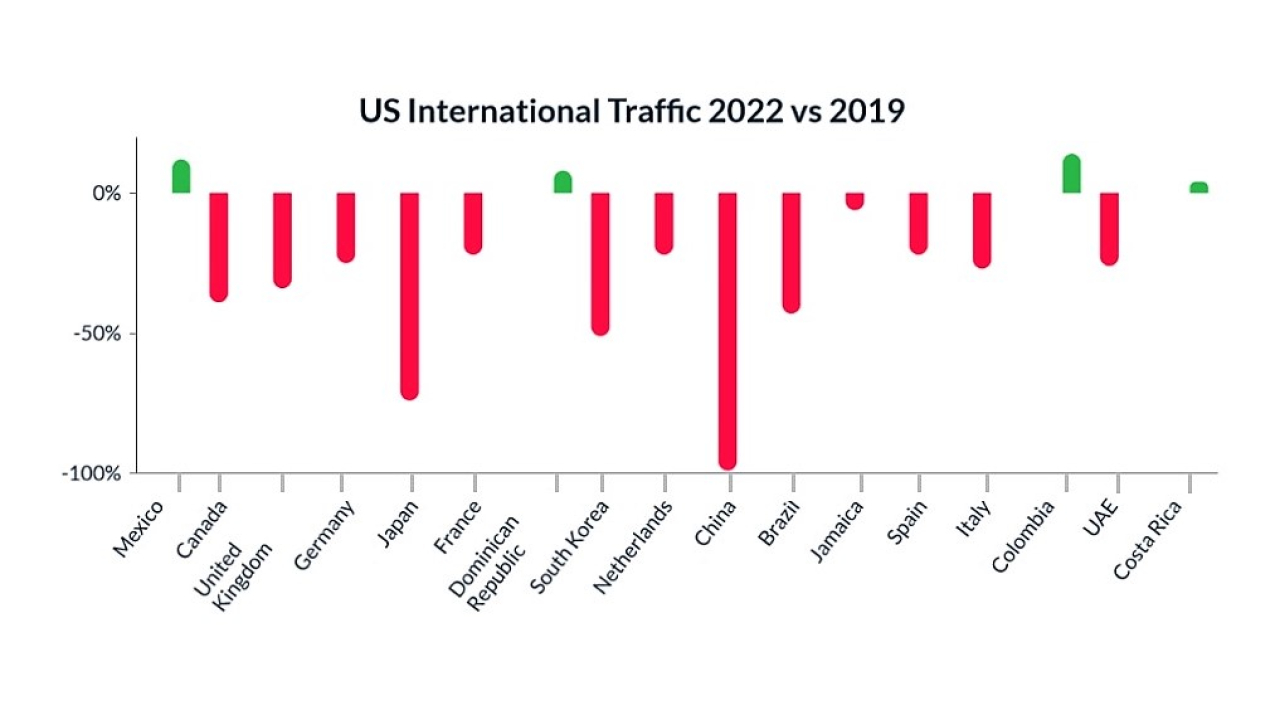

Currently, the difference is exceptionally high (see chart below) as United States-Canada traffic was still around 40% below 2019 numbers in 2022 while air traffic between Mexico and the U.S. was 12% up. Mexico now makes up a quarter of all U.S. international traffic. Meanwhile, due to the slow removal of travel restrictions, Asian countries like Japan and China are still far from their pre-pandemic volumes.

Mexico saw swift share gains during the pandemic.

© Dion Zumbrink

Mexico is among only four countries where U.S. air traffic was above pre-pandemic levels last year. The others were Dominican Republic (8%), Colombia (14%), and Costa Rica (4%) and it is evident that tourism is a major contributing factor to the recovery of these international destinations.

While Mexico is well ahead post-pandemic, if we look at the historical growth of United States-Mexico traffic, it has nearly doubled since 2010. This trend has been in the making for a long time and below we assess the main factors contributing to today’s accelerated growth of this market and the potential to sustain the trend. We start with the airlines.

Just four air markets were in positive territory in 2022 versus 2019.

© Dion Zumbrink

American Carriers Take Back Share

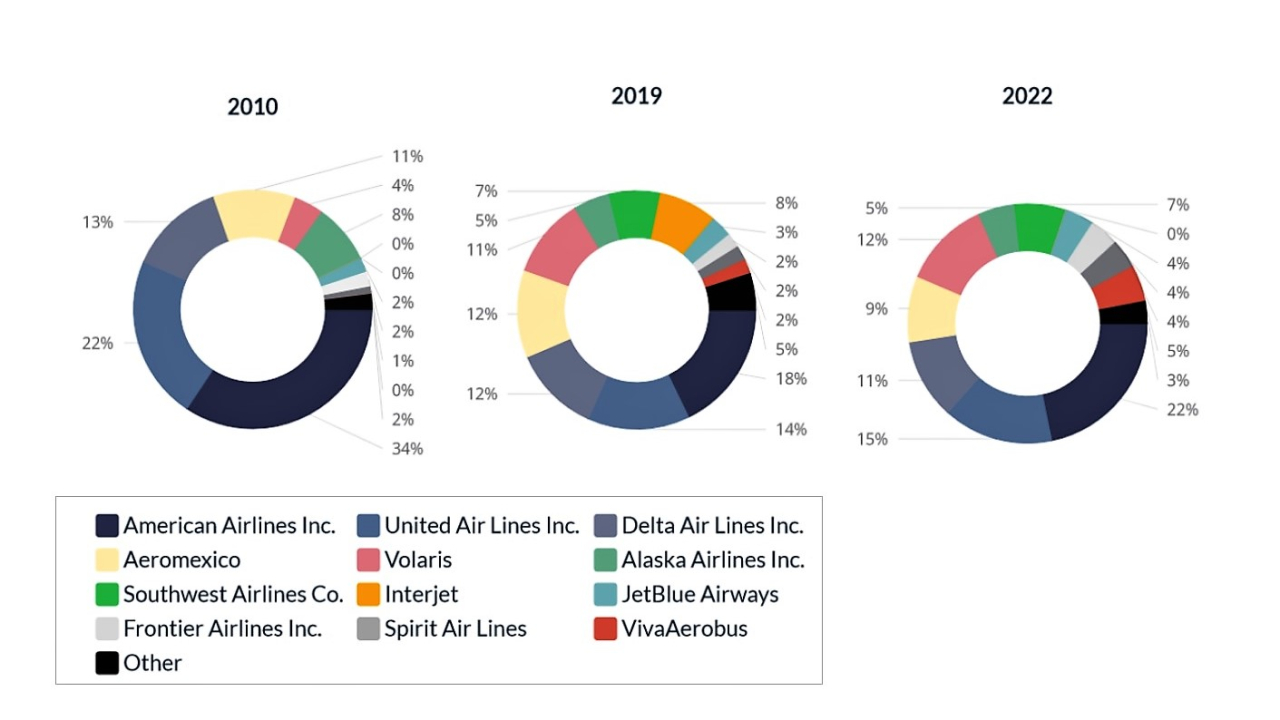

Twelve airlines have been active in the market at a large scale, but it is mainly low-cost carriers (LCCs) and ultra-low-cost carriers (ULCCs) that have expanded capacity in the last decade. The market share of full-service carriers decreased dramatically from 80% in 2010 to 56% in 2019.

In 2010, the three main U.S. legacy carriers together had a market share of nearly 70% which had shrunk to just 44% by 2019. In 2022, this increased again (but remained under the 50% mark) mainly aided by the expansion of American and United Airlines.

The growth between 2019 and 2022 has come mainly from U.S. carriers. American Airlines grew significantly post-pandemic, taking over a fifth of the market once again. It has strengthened its leading position having seen its share drop below 20% due to a declining trend earlier in the decade.

American carriers have increased their share after years of contraction.

© Dion Zumbrink

The Mexican bump appears to be part of the airline’s wider strategy of expansion in Latin America and South America. The second largest airline, United, also slightly increased its share, while Delta has drifted back a little.

In terms of LCCs, Southwest, Alaska, and JetBlue carried an additional 11%, 16%, and 39% of passengers respectively. However, the largest relative growth has come from the ULCCs Frontier and Spirit which have doubled their share of the market compared to 2019.

On the Mexican side, ULCCs have also been a driving force, namely Volaris, and VivaAerobus, with the latter more than quadrupling its traffic versus 2019, and increasing its share. However, the overall volume of passengers carried on Mexican airlines is still below the 2019 level. This is partly due to the airline Interjet ceasing operations, having been the sixth-largest airline in the market in 2019.

Another major reason is that in May 2021, the FAA downgraded Mexico’s air safety rating from Category 1 to 2 as, according to the FAA, it did not meet ICAO standards. This meant that Mexican airlines could not open new routes or expand capacity on existing ones. The Mexican government is reportedly working on upgrading to Category 1 this year.

If that happens it would likely significantly boost the capacity of Mexican carriers. Aeromexico, Volaris, and VivaAerobus are expected to grow their total network seat capacity, leading to a total increase of almost 40% by 2027. All three airlines have large outstanding aircraft orders: Viva is likely to have a fleet of 92 planes by 2025, up from just 37 before the pandemic, and Volaris is set to go from 82 in 2019 to 160 in 2027.

In Part 2 of this report (to be published on 24 May) we will look at United States-Mexican city pairs and discover what is behind the growth of the top destinations, and why some locations are winning but not others.