Login/Register

Why the Asia-Pacific Airport PPP Market Remains a Good Bet [Part 2 of 2]

Curtis Grad

November 29, 2023

Beijing Capital Airport.

© AcidBomber / Wikipedia

Last week, in part one of this article, we looked at the airport public-private partnerships (PPPs) in India and the Philippines that were at the forefront of the Asia-Pacific market. Here let’s delve a little into the investment side.

Stocks and shares are an indicator of current investor mood. Among the handful of listed airport operators in Asia-Pacific—including Auckland Airport, Beijing Capital Airport Company, Japan Airport Terminal, Shanghai Airport (Avinex), and Airports of Thailand—performances to the end of November have been very mixed.

China’s Top-Listed Operators Struggle

Across these five companies, year-to-date share prices (to 30 November) indicate that only Auckland International Airport delivered growth with its stock slightly ahead by 3.2%, and Japan Airport Terminal Company the next best, down by 0.9% (source MarketWatch).

In sharp contrast, Beijing Capital International Airport Company was heavily down by 50.1%, while its mainland rival, Shanghai International Airport Company, also performed poorly, dropping 37.4%. Both stocks are the lowest they have been in several years as they suffer from China’s weakened economy. GDP has been revised down to 5% this year, and 4.5% in 2024, according to a Reuters poll.

“This slowdown could be just the tip of the iceberg,” Bingnan Ye, senior economist at China Merchants Bank International in Hong Kong told the agency. He said the downside risk was that household consumption might improve “more slowly than many expect.”

Moreover, the elation surrounding China reopening its borders in January has been tempered by the fact that travel activity is still low. According to travel analyst, ForwardKeys, neither Beijing Capital nor Shanghai Pudong will make the global top 10 for departure scheduled seats for the 12 months to February 2024.

Meanwhile, Airports of Thailand – whose international gateways have traditionally been reliant on Chinese travelers – has seen its shares fall by 21.3% year-to-date, a decline that really only started around mid-November. After a bumpy ride during COVID19, the stock had performed well from January 2022 with a solid upward trend overall until this month’s sharp drop.

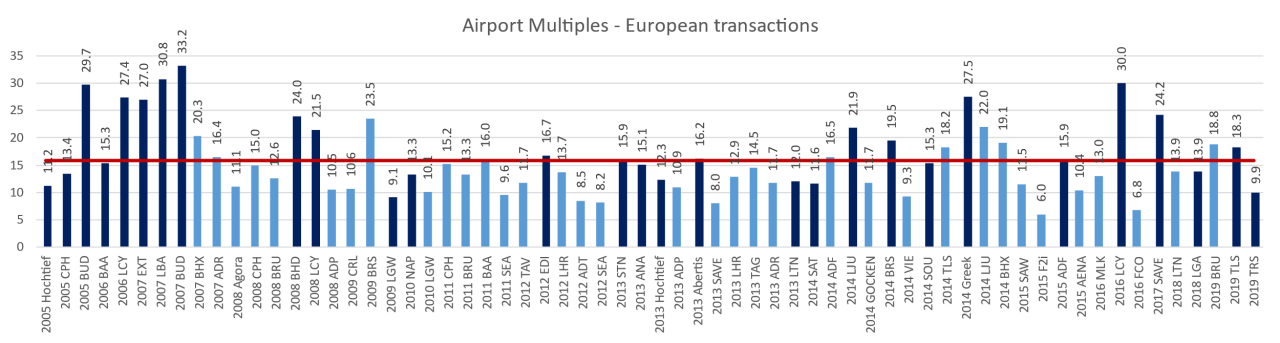

Dark blue = majority share stakes, Light blue = minority share stakes

© Modalis Infrastructure Partners

In the world of infrastructure, airports have been a good financial bet in the past. Modalis Infrastructure Partners recently updated its analysis of EBITDA multiples for selected airports and operators broken down by majority share stakes (in dark blue) and minority share stakes (in light blue).

As the chart above shows, the average EBITDA multiple was 15.9 but early majority-stake deals have outperformed this, sometimes by close to double (or more). After the global financial crisis in 2008-09, multiples slipped dramatically and there was extra caution in the market with more minority (rather than majority) deals taking place.

In general, however, EBITDA multiples for majority stakes have performed better, with London City Airport (LCY), Fraport’s Greek Airports, and Italy’s SAVE showing some strong gains since 2014.

To List or Not to List?

In March, Australian investment management firm Maple-Brown Abbott released an analysis comparing the average trading multiple of listed airport companies versus the average direct transaction multiple over the past decade.

The firm reviewed 35 transactions of global airports over the 10 years from 2013 to 2022. It found an average transaction multiple over this time was 17.0x EV/EBITDA, which represents a 35% premium to the average trading multiple of listed airports of 12.6x.

Why would there be this historical out-performance of unlisted over listed infrastructure? There are several reasons, both structural and circumstantial.

Maple-Brown Abbott said: “In our view, the combined tailwinds of greater leverage, rising asset prices, and a widening valuation gap between assets in the listed and direct markets have been the major contributors. Many of these tailwinds are unlikely to continue indefinitely and some appear to have been caused by short-lived factors including a historical period of declining and low interest rates.”

In the airports sector, there is also the stability factor of large gateways being fully owned by the state to consider. In parts of the world such as the United States, the Middle East, and parts of Asia, this is the case, even though some, such as Singapore Changi Airport (SIN), operate at arms-length under a private business model. This can offer the best of both worlds: state financial coffers—useful during events such as the Global Financial Crisis and COVID—but still run on a profit principle.

Nevertheless, airport privatization through PPP continues to have a valuable place. It offers governments a route to new—and regular—revenue streams over a long contract period; better-managed facilities, as they are often taken over by highly skilled global operators, sometimes in partnership with local infrastructure players; and a viable route to mid- and long-term investment via capital markets, allowing facilities to stay up-to-date through infrastructure development.

Some airports like Singapore Changi Airport, operate at arms-length from government under a regular business model.

© Changi Airport Group

Major acquirers, whether individual companies or consortia, are also more likely to actively manage the business, cut costs and improve efficiencies. All of these can improve profitability and appeal to shareholders as well as ratings agencies, an important factor when considering the cost of debt for new projects.

In a post-COVID market, we have seen air traffic recovering at different rates in different regions depending on their speed of opening up to international travel; persistent consumer appetite for travel abroad; but also the cost-of-living crisis limiting discretionary spending. The general trend for air traffic, however, is firmly back up again.

ACI data show that major international hubs, in particular, boomed in 2022. Dubai (DXB), for example, saw its traffic soar by 127% pushing the airport up to fifth place in the global ranking (from 27th in 2021). Even more spectacular was London Heathrow (LHR), rising from 54th to eighth on the back of 218% passenger growth. Asian airports were, however, largely missing from the list, apart from Delhi’s Indira Gandhi International Airport (DEL) ranked ninth, and Tokyo Haneda (HND) ranked 16th. This year, more Asia-Pacific airports should return to the top 20.

The normalization of air travel in 2023 and 2024 will be a stabilizing influence on the market and a signal for stalled privatization projects to proceed again. Investors will always look at the numbers first and if the demand forecasts for cargo and passengers are back on track for the next decade, so will their appetites.

Modalis Infrastructure Partners expects to see a steady flow of deals in Asia-Pacific in the next 12-18 months as passenger numbers rise on the rebound of discretionary spending, with capacity constraints again becoming an issue, and general market confidence returning.

[This is an updated version of an article that first appeared in the November 2023 issue of ACI’s Airport World magazine.]