in

Adani Airports

9

Airports

1

Country

8

Reports

Login/Register

Terminal 2 at Mumbai's Chhatrapati Shivaji International Airport. operated by Adani-majority-owned Mumbai International Airport Limited.

© Adani Enterprises

in

Airports

Country

Reports

sg

Airports

Countries

Reports

gb

Airports

Countries

Reports

in

Airports

Countries

Reports

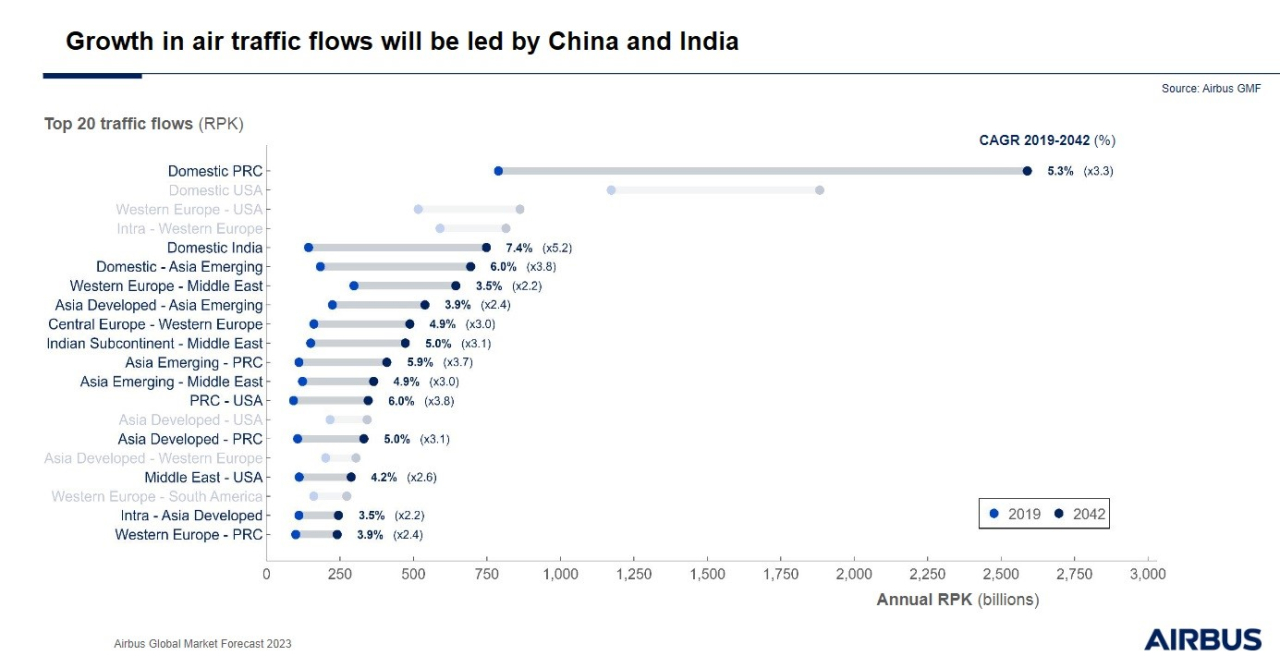

Despite being very slow to remove COVID restrictions, Asia-Pacific remains a key region for airport investment and development as traffic flows are predicted to see some of the biggest rises in the coming years. This is especially so for domestic travel in China and India, based on Boeing’s outlook to 2042.

Largely, this has been driven by demographic shifts in terms of population growth as well as wealth creation which has taken more people into the middle-class segment, who then have the means—and inclination—to travel.

According to data sourced by Statista, Asia-Pacific’s already large middle-class population—1.38 billion in 2015 versus Europe’s 724 million—is set to explode to 3.49 billion by 2030. Meanwhile, numbers in the developed regions of North America and Europe will be stagnant. Even other developing regions like Central and South America; the Middle East and North Africa; and Sub-Saharan Africa are not expected to show anything like the growth of Asia-Pacific in the coming decade.

Airports in the region are expected to benefit hugely from this growth, which is why governments and private operators are planning ahead to ensure that their respective facilities are equipped to meet the future high demand for air travel. India provides a great example of this as the most populous country in the world has been on a privatization path for over 15 years.

State-owned Airports Authority of India has handed over control of multiple assets, mainly through public-private partnership (PPP) contracts, to local players such as GMR and GVK, initially with the latter divesting its airport holdings, including Mumbai (BOM) and the planned Navi Mumbai, to Adani in mid-2020.

As highlighted in the AirportIR Deal Pipeline, this process is still ongoing with a second phase of airport privatizations that will see 25 more airports put out to bid based on the mood music from India’s aviation ministry. Most of these are regional brownfield gateways with a total passenger throughput of 13 million, and the contract length is expected to be 50 years.

While India is perhaps the most active market in Asia-Pacific for PPP activity, other major ‘live’ projects are scattered across the region, from Pakistan in the west; Indonesia and the Philippines; and Australia in the east.

At the end of last year, local media reported that there was a green light for Pakistan’s Aviation Ministry to begin outsourcing operations of Jinnah International Karachi Airport (KHI), Islamabad International Airport (ISB), and Allama Iqbal International Airport (LHE) under a PPP model.

The Ministry tweeted on X (formerly Twitter) that outsourcing would “pave the way for foreign direct investment” which could help improve standards and services at the airports under contract(s) that would run for 20 to 25 years. In June, however, the government stepped back, saying it would restrict the outsourcing to ISB for the time being, preferring a cautious, step-by-step approach.

All change in the Philippines for Manila's main airport.

© patrickroque01 / Wikipedia

In the Philippines, several airports are in a privatization queue, but the big one is Manila’s Ninoy Aquino International Airport (MNL), which handled almost 48 million passengers in 2019. Unsolicited bids were made in recent years with the latest, according to a local report in June, coming from the Manila International Airport Consortium. Its proposal is $4.7 billion (Ps267 billion) for a 25-year concession rather than 15 years.

The consortium – composed of Aboitiz InfraCapital, AC Infrastructure Holdings Corp, Asia’s Emerging Dragon Corp, Alliance Global – Infracorp Development, Filinvest Development Corp, JG Summit Infrastructure Holdings Corp, and Global Infrastructure Partners – said a shorter concession would lead to higher passenger charges and lower investment.

The MNL project is structured in two phases: improvements and enlargement of the existing terminals, and expanding capacity to 65mppa within a four-year period. By September, at least five companies had secured bid documents, but eight bidders are expected by the December 27 deadline.

Meanwhile, at Sangley Point (SGL), the conversion of the Atienza navy base to a civilian airport costing $11 billion, looks like it could move forward. A local report said that the Virata-Yuchengco-led consortium signed a joint venture and development agreement with the Cavite provincial government. Other partners include Samsung C&T Corp, as well as MacroAsia Corp (in a non-equity capacity).

Manila’s new northern gateway, Bulacan International Airport, is well into its construction phase. The PPP project is led by SMC whose subsidiary San Miguel Aerocity Inc was granted the franchise to construct and operate the new international gateway following an unsolicited bid. According to the government, the four-runway airport should begin operations in 2027 and have a capacity of 200 million passengers per year.

As all of these projects are in the greater Manila metro area, they will impact the scope/viability of each other so careful consideration of the terms of each deal will be required on all sides to get the best out of these assets.

[The second part of this article will focus on the investment side of the PPP market in Asia and it will be published on AirportIR on November 29. If you can’t wait that long, the full article can be read in the November 2023 issue of ACI’s Airport World magazine.]