Login/Register

Ultra-low-cost Carriers Now Have a Double-digit Market Share in the U.S.

Dion Zumbrink

February 28, 2024

Livery on Spirit's A319.

© Spirit Airlines

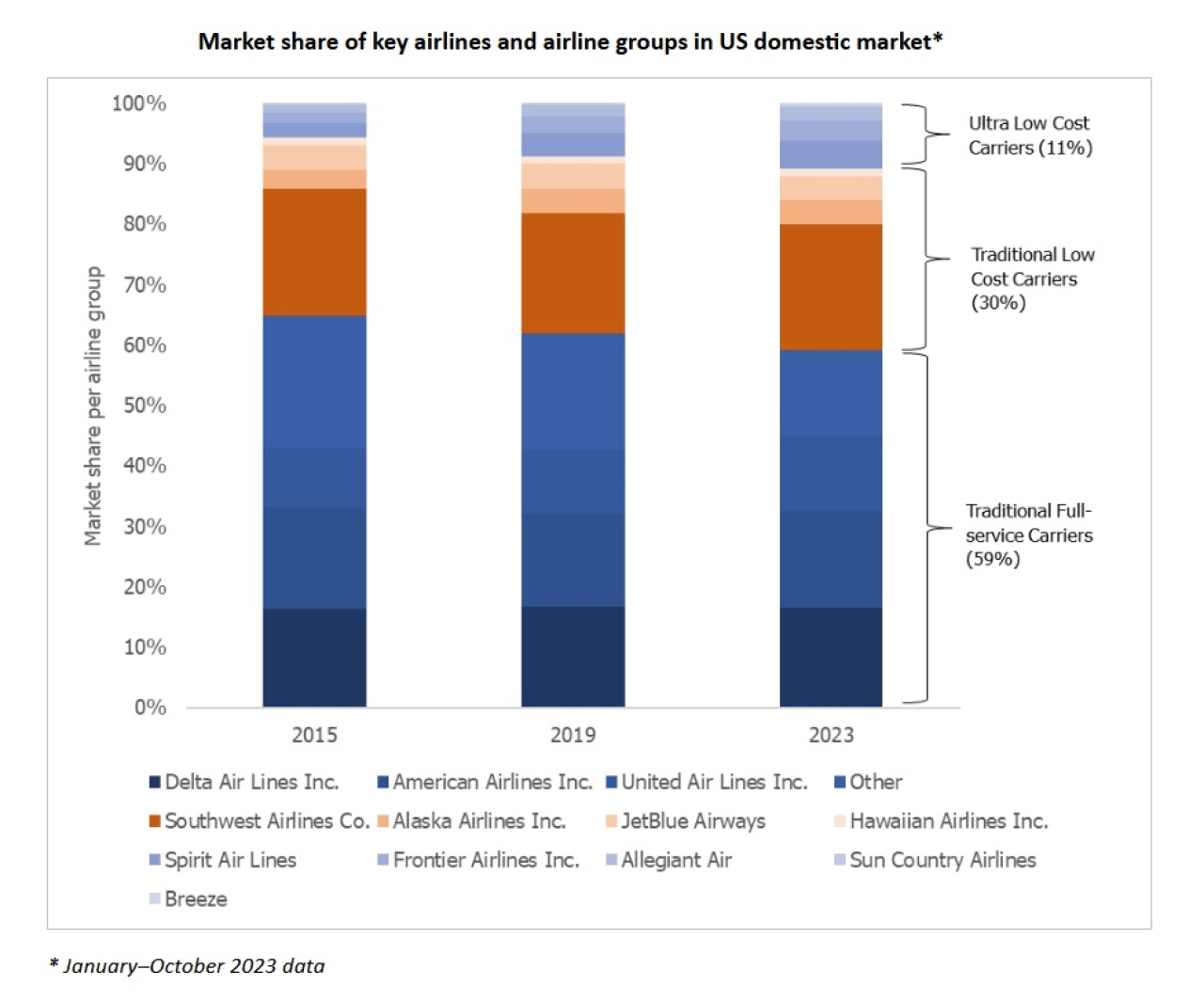

In 2023, ultra-low-cost carriers (ULCCs) in the United States continued the growth trend initiated in the previous decade. The market was led by Spirit, with the largest share, and accompanied by a new airline, Breeze, which began operations in 2021.

At the outset, the business model appeared to be successful, stimulating the domestic market and seeing double-digit growth rates between 2015 and 2023. In this time frame, the market share of ULCCs in the U.S. domestic market has grown from 6% to 11%, mainly at the cost of traditional full-service carriers. Existing low-cost carriers maintained their share of roughly 30%.

© Dion Zumbrink

The passenger growth alone, however, does not tell the whole story as profitability of ULCCs is under pressure. Various operational issues have had an impact on the margins of ULCCs—to a greater extent than legacy carriers. Therefore, mergers have been sought to more easily battle the market leaders in the American aviation market.

The recent ruling of a federal judge declaring the Jetblue–Spirit merger anti-competitive may prove to be fatal for the largest ULCC in the country.

But how does this affect the airports in the country?

The growth of ULCCs can have a positive impact on airports due to the opening of new routes, more competition on routes which lowers ticket prices, and wider availability of options. All of this can drive passenger numbers upwards.

On the other hand, any mergers will lower competition but not necessarily seat volumes and route networks—if both brands continue to operate independently. It does, however, reduce the negotiating position of airports if they are dealing with stronger consolidated airlines.

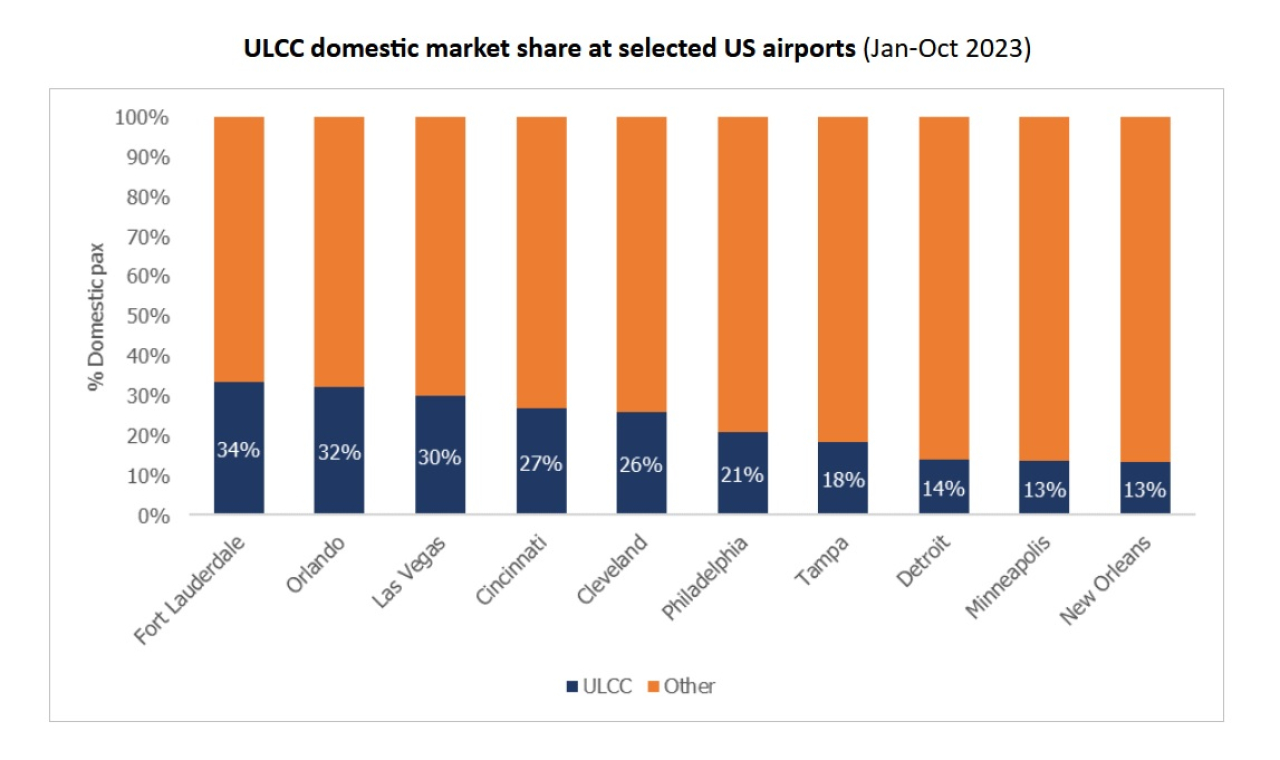

As can be seen below, the main airports with above-average domestic passengers using ULCCs are medium-sized hubs and tourism destinations. However, even there, the market share of ULCCs never reaches much above a third of the market as is the case at Fort Lauderdale Airport.

© Dion Zumbrink

Interestingly, while in Europe many smaller airports are dominated by a ULCC such as Ryanair or Wizz Air, with over 80% market share, this is not the case in the United States.

The largest airports in the country all have ULCC participation at well below 10%, except Denver which recorded 11% last year. Even at smaller airports with under five million annual passengers, the ULCC market share tends to lie below 20%.

Limited Exposure

At these participation rates, the majority of airports would only be marginally affected by any changes in the composition of the airline mix. Most U.S. airports have a sufficiently extensive mix of airlines to limit their exposure to the variability of ULCCs though, from a general airport perspective, it is favorable to have a multitude of airline brands and business models in operation.

Despite the challenges, ULCCs expect to continue growing, and Spirit claims financial solvency while also appealing to the federal ruling on its merger with Jetblue.

Sun Country continues to grow its fleet in 2024 and Frontier expects its capacity to increase by between 12%-15%. Allegiant is more conservative with 1% expected growth in available seat miles in 2024 but overall, the market sector remains growing. Breeze, the latest and smallest of the ULCCs, also continues its expansion with an expected 12 new aircraft in 2024, serving 25 new routes.

The market share of ULCCs at U.S. airports should therefore carry on growing at a steady pace in the near future.