Login/Register

COVID-HQ: The Marathon Nature of the Pandemic is Becoming Clearer in this Final Article of the Series

Frode Skulbru

June 29, 2020

(Note: This analysis is the last in a series spanning 15 weeks)

June 29, 2020

The Marathon Nature of the Pandemic is Becoming Clearer in This Final Article of This Series

By Frode Skulbru (Vancouver, Canada) All (good) things come to an end, and this 15th article in this series will be the final for now. After dramatic shifts over the last four months, we have now entered a new phase with re-openings in parts of the world, sharp increases of new cases in other parts and possibly second waves of the pandemic in yet other parts. The fast out of the gates sprint comes to an end now that more and more people realize this was never a sprint, but a marathon. Capacity As usual we start with the capacity situation first. OAG reports that the first official week of summer has resulted in the largest week on week growth in capacity during the Covid-19 event with some 8.2 million seats added back around the globe and a week on week percentage increase of 21%. Demand may not respond as quickly, however this is a good indication going forward. Capacity now stands at 41% of that available in the same week last year which is around seven percentage points up from last week.  Source: OAG Stock Market The share prices of our select companies remain to follow the same pattern as all stocks declined in value last week. With the V shaped recovery of the stock market now slowing down, economic reality might finally be in the process if caching up with the market as even the exchanges listed here had a negative week.

Source: OAG Stock Market The share prices of our select companies remain to follow the same pattern as all stocks declined in value last week. With the V shaped recovery of the stock market now slowing down, economic reality might finally be in the process if caching up with the market as even the exchanges listed here had a negative week.  Compared to the year’s high in January, March was the low point in terms of value followed by a sharp fall of aviation demand in April. The following table lists the share values at the end of each month since February. Whereas most exchanges are within striking distance of an all time high, aviation related stocks still offer a deep discount.

Compared to the year’s high in January, March was the low point in terms of value followed by a sharp fall of aviation demand in April. The following table lists the share values at the end of each month since February. Whereas most exchanges are within striking distance of an all time high, aviation related stocks still offer a deep discount.  The airport companies in the graph below experienced a sharp drop in March, same as the overall market. A decent recovery in April and into May has now been replaced with a slight decline and a continuation of the “holding pattern” we mentioned last week. Not surprisingly, the airline values have a similar pattern maintaining an even deeper loss than the airports so far this year.

The airport companies in the graph below experienced a sharp drop in March, same as the overall market. A decent recovery in April and into May has now been replaced with a slight decline and a continuation of the “holding pattern” we mentioned last week. Not surprisingly, the airline values have a similar pattern maintaining an even deeper loss than the airports so far this year.  Traveler Confidence Key to Recovery Pending an effective treatment and/or vaccine, re-building passenger confidence around a series of mitigating measures based on any given country’s health recommendation seem to be the approach taken by most airports and airlines. The various aviation organizations are recommending similar approaches, although there does not seem to be one accepted standard across airports and airlines at this point. There is a lot of talk about the “new normal”, but there cannot be a new normal before there is a stability in the pandemic, a trust that one can travel relatively safely and that one will not be quarantined in any given country due to a sudden outbreak. For airports, there is a long way to go before any “new normal” can be established. The number of moving parts is still vast and will continue to pull in opposite direction depending on which point in time airport managers are planning for. If, for example, the new normal requires a continuation of the physical distancing rules into the foreseeable future, many airports would require mores space for line-ups and waiting areas than they have today in order to attract the same number of passengers as the pre-COVID aera. In the short term, there should not be an issue as the demand is not present. however, in the longer term funds for expanding facilities or even re-purposing areas within a terminal are simply not there due to the industry losses so far. ACI recently released a comprehensive report titled “Aviation Operations During COVID-19 Business Restart and Recovery” where it outlines the challenges and makes recommendations for the way forward. The report clearly illustrates the complexity of a planned and efficient recovery. In one of our previous articles, Modalis graphically illustrated the number of organizations that would need to have input into an Airport Public Health Preparedness Contingency Plan (or whatever title various airports may come up with).

Traveler Confidence Key to Recovery Pending an effective treatment and/or vaccine, re-building passenger confidence around a series of mitigating measures based on any given country’s health recommendation seem to be the approach taken by most airports and airlines. The various aviation organizations are recommending similar approaches, although there does not seem to be one accepted standard across airports and airlines at this point. There is a lot of talk about the “new normal”, but there cannot be a new normal before there is a stability in the pandemic, a trust that one can travel relatively safely and that one will not be quarantined in any given country due to a sudden outbreak. For airports, there is a long way to go before any “new normal” can be established. The number of moving parts is still vast and will continue to pull in opposite direction depending on which point in time airport managers are planning for. If, for example, the new normal requires a continuation of the physical distancing rules into the foreseeable future, many airports would require mores space for line-ups and waiting areas than they have today in order to attract the same number of passengers as the pre-COVID aera. In the short term, there should not be an issue as the demand is not present. however, in the longer term funds for expanding facilities or even re-purposing areas within a terminal are simply not there due to the industry losses so far. ACI recently released a comprehensive report titled “Aviation Operations During COVID-19 Business Restart and Recovery” where it outlines the challenges and makes recommendations for the way forward. The report clearly illustrates the complexity of a planned and efficient recovery. In one of our previous articles, Modalis graphically illustrated the number of organizations that would need to have input into an Airport Public Health Preparedness Contingency Plan (or whatever title various airports may come up with).  Clearly, the task at hand is not solved overnight. A place to start could be with an “aviation health and audit assessment” as defined and offered by Modalis. This is a structured approach to navigating though the rules and guidance to ensure compliance, followed by a plan for implementation.

Clearly, the task at hand is not solved overnight. A place to start could be with an “aviation health and audit assessment” as defined and offered by Modalis. This is a structured approach to navigating though the rules and guidance to ensure compliance, followed by a plan for implementation.  More info can be requested from the Airport QM website or LinkedIn. Direct contact at: [email protected] Returning to the topic of passenger confidence, IATA recently released results from a survey about the potential travel plans for respondents after the pandemic has subsided.

More info can be requested from the Airport QM website or LinkedIn. Direct contact at: [email protected] Returning to the topic of passenger confidence, IATA recently released results from a survey about the potential travel plans for respondents after the pandemic has subsided.  The post-COVID recovery in the air transport industry has three critical elements; the containment of the pandemic, the loosening of travel restrictions and border closures and, critically, the restoration of passenger confidence to resume flying. The above chart presents the updated (June) findings of an IATA-commissioned survey of passengers across 11 countries to understand their views on the likely timing of a return to air travel. The decline in respondents plans to travel within the first 1-2 months is sobering and likely confirms the industry’s broader view that the industry recovery will begin in Q3 2020 but that it will be gradual in nature. Nonetheless, the survey highlights one of the important risks to our recovery profile, with more than half of travelers indicating that they will not fly until at least the end of the year if not into 2021. While passengers are worried about a range of factors, among the measures that would make passengers feel safer are that airport and aircraft staff wear appropriate PPE and that airport and aircraft facilities are regularly cleaned and sanitized. Understanding and addressing the concerns of passengers, and communicating these initiatives effectively, will be vital to the restoration of consumer confidence in air travel and getting the industry back flying again. At the same time, the world reported 1,292,886 new confirmed cases, up from 949,952 the previous week. The number of fatalities was 36,230 this week, an increase of 4,814 compared to last week (31,416). Stay Safe – Be Kind – Take Care

The post-COVID recovery in the air transport industry has three critical elements; the containment of the pandemic, the loosening of travel restrictions and border closures and, critically, the restoration of passenger confidence to resume flying. The above chart presents the updated (June) findings of an IATA-commissioned survey of passengers across 11 countries to understand their views on the likely timing of a return to air travel. The decline in respondents plans to travel within the first 1-2 months is sobering and likely confirms the industry’s broader view that the industry recovery will begin in Q3 2020 but that it will be gradual in nature. Nonetheless, the survey highlights one of the important risks to our recovery profile, with more than half of travelers indicating that they will not fly until at least the end of the year if not into 2021. While passengers are worried about a range of factors, among the measures that would make passengers feel safer are that airport and aircraft staff wear appropriate PPE and that airport and aircraft facilities are regularly cleaned and sanitized. Understanding and addressing the concerns of passengers, and communicating these initiatives effectively, will be vital to the restoration of consumer confidence in air travel and getting the industry back flying again. At the same time, the world reported 1,292,886 new confirmed cases, up from 949,952 the previous week. The number of fatalities was 36,230 this week, an increase of 4,814 compared to last week (31,416). Stay Safe – Be Kind – Take Care

June 22, 2020

By Frode Skulbru (Vancouver, Canada) In this 14th week of this series of articles we observe that some of the positive changes and value increases have lost steam as pandemic numbers are growing again, large scale demonstrations have taken place and a wait and see attitude seems to have gotten a foothold in the market. Society and the economy are slowly opening in some parts of the world while other areas are now in the epicentre of the pandemic. Capacity Worldwide, the number of scheduled flights compared to the same week in 2019 remain 62.9% below and roughly at par with last week. As the pandemic has hit various parts of the globe at different times, the traffic reduction has remained in the mid-60s % below last year since April. Countries with no domestic traffic remain with an over 90% loss in activity since last year. Hong Kong and Singapore are examples of this.  Source: OAG Stock Market Eleven of the 13 stocks tracked in this series of articles lost value last week. The six airport companies all lost value for the second week in a row illustrating the concern in the market about multiple moving parts like the procedure of re-opening the aviation market, new health regulation for travelers, continuous quarantine rules, anti-racist demonstrations, reports of higher than ever new cases per day and the economy in general.

Source: OAG Stock Market Eleven of the 13 stocks tracked in this series of articles lost value last week. The six airport companies all lost value for the second week in a row illustrating the concern in the market about multiple moving parts like the procedure of re-opening the aviation market, new health regulation for travelers, continuous quarantine rules, anti-racist demonstrations, reports of higher than ever new cases per day and the economy in general.  Year to date, the situation remains similar to last week, albeit with a slight decline. The general increase that was observed from mid-May seems to have stagnated and we are now in a holding pattern.

Year to date, the situation remains similar to last week, albeit with a slight decline. The general increase that was observed from mid-May seems to have stagnated and we are now in a holding pattern.  Although all the airport stocks are priced higher today compared to May 18th, the last two weeks have been relatively flat. The 8th of June was the high point so far across the board for the airports, illustrating again the global connectivity of the issues at hand.

Although all the airport stocks are priced higher today compared to May 18th, the last two weeks have been relatively flat. The 8th of June was the high point so far across the board for the airports, illustrating again the global connectivity of the issues at hand.  At the same time, the world reported 949,952 new confirmed cases, up from 1,003,242 the previous week. The number of fatalities was 31,416 this week, down 1,818 compared to last week (33,234).

At the same time, the world reported 949,952 new confirmed cases, up from 1,003,242 the previous week. The number of fatalities was 31,416 this week, down 1,818 compared to last week (33,234).

June 15, 2020

Previous weeks value increases lost amidst concerns of impact of demonstrations and complicated rules around safe and healthy travel initiatives

By Frode Skulbru (Vancouver, Canada) In last week’s article we reported a growth in share-prices across the board. This week, the opposite is the case as all tracked assets except LAN lost value between June 8 and June 15. All assets, except Fraport, are however showing an increased share-price so far in June. LAN remains the best performer at 144.2% for the month, although the airline still 72% down year-to-date. Among the airports, Beijing is up 20.7% so far this month, with Fraport being down 5.2%.  Capacity Although many carriers are now announcing plans to increase capacity in the coming months (e.g. statements like “WestJet will double the number of flights in July vs. June”), overall capacity remained largely unchanged last week.

Capacity Although many carriers are now announcing plans to increase capacity in the coming months (e.g. statements like “WestJet will double the number of flights in July vs. June”), overall capacity remained largely unchanged last week.  Source: OAG

Source: OAG  Source: ICAO Year to Date Share Price Developments Given the set-back reported for the week, the overall recovery for 2020 has slowed. Airports of Thailand remain closest to the January value, being 16.9% down for the year.

Source: ICAO Year to Date Share Price Developments Given the set-back reported for the week, the overall recovery for 2020 has slowed. Airports of Thailand remain closest to the January value, being 16.9% down for the year.  Examples of Continuing Restrictions Although general restrictions are slowly lifting in some countries whereas others are still under strict lock-down regulations, the limitations of international travel remain similar across the board but with broader exceptions as the three panels below as published by ICAO indicates. Santiago, Chile is currently under lock-down. In general, the borders are closed for foreign nationals. his is similar for China, but here passengers from Hong Kong and Taiwan are allowed. Passengers with travel visas issued after March 28th, 2020, presumably as these pax have been screened and found healthy. Norway went through a lock-down for a period of time, but is now allowing passengers from Finland, Iceland, Greenland, The Faroe Islands, Gotland, the Aaland Islands and Denmark. All other passengers will be tuned away at the border. The potential positive signal with the above is that it seems like as domestic travel recovers, there is an easing of international travel from select international destinations.

Examples of Continuing Restrictions Although general restrictions are slowly lifting in some countries whereas others are still under strict lock-down regulations, the limitations of international travel remain similar across the board but with broader exceptions as the three panels below as published by ICAO indicates. Santiago, Chile is currently under lock-down. In general, the borders are closed for foreign nationals. his is similar for China, but here passengers from Hong Kong and Taiwan are allowed. Passengers with travel visas issued after March 28th, 2020, presumably as these pax have been screened and found healthy. Norway went through a lock-down for a period of time, but is now allowing passengers from Finland, Iceland, Greenland, The Faroe Islands, Gotland, the Aaland Islands and Denmark. All other passengers will be tuned away at the border. The potential positive signal with the above is that it seems like as domestic travel recovers, there is an easing of international travel from select international destinations.

The other common thread is that all passengers must comply with the health and sanitary requirements issued by the health authority. The challenge internationally is that, although similar, common and uniform procedures across international borders have not been developed. Please see our separate article on this topic here. At the same time, the world reported 1.003.292 new confirmed cases, up from 819,008 the previous week and one of the highest weekly number reported to date. The number of fatalities was 33.234 this week, up 2,383 compared to last week (30,851). The WHO reported that Sunday June 8th had the highest number of new cases reported since the beginning of the pandemic. Nearly 75 per cent of Sunday’s cases originated from 10 countries, mostly in the Americas and South Asia, WHO Director-General Tedros Adhanom Ghebreyesus said during a media briefing in Geneva, noting that countries in the African region are beginning to see an increase in cases.

The other common thread is that all passengers must comply with the health and sanitary requirements issued by the health authority. The challenge internationally is that, although similar, common and uniform procedures across international borders have not been developed. Please see our separate article on this topic here. At the same time, the world reported 1.003.292 new confirmed cases, up from 819,008 the previous week and one of the highest weekly number reported to date. The number of fatalities was 33.234 this week, up 2,383 compared to last week (30,851). The WHO reported that Sunday June 8th had the highest number of new cases reported since the beginning of the pandemic. Nearly 75 per cent of Sunday’s cases originated from 10 countries, mostly in the Americas and South Asia, WHO Director-General Tedros Adhanom Ghebreyesus said during a media briefing in Geneva, noting that countries in the African region are beginning to see an increase in cases.

June 8, 2020

Share Prices Keep Increasing Among Rising Cases & Massive Demonstrations

By Frode Skulbru (Vancouver, Canada) In late March, global capacity shed around three million seats per day. In the last two weeks capacity has increased by just over 440,000 seats per day, indicating the start of a real recovery albeit there is a long, 78 million seats to go. Consumer confidence remains a key issue as airlines, airports and other stakeholders are beginning to explain exactly how flying will be safer than ever. Countries without domestic traffic continue to show very low numbers, with Hong Kong and Singapore being the best examples in the below table from OAG.  Source: OAG Globally, we observe a slight increase this past week. More concerning is the fact that confimed new cases reached a new high Sunday June 7th.

Source: OAG Globally, we observe a slight increase this past week. More concerning is the fact that confimed new cases reached a new high Sunday June 7th.  Source: ICAO Turning to the share prices of our tracked assets where every single asset increased in value over the last week. The clear winner is LAN at a whopping 142.5%, albeit from a low base. All the airport companies are showing healthy growth, illustrating a longer turn optimism by investors as most of these still have very limited traffic to defend the increases.

Source: ICAO Turning to the share prices of our tracked assets where every single asset increased in value over the last week. The clear winner is LAN at a whopping 142.5%, albeit from a low base. All the airport companies are showing healthy growth, illustrating a longer turn optimism by investors as most of these still have very limited traffic to defend the increases.  In a (virtual) conference in Dallas last week, ACI World Economics Director Patrick Lucas presented a quasi-U-shaped / L-shaped recovery model. Despite the early and promising signs of capacity recovery, ACI is now looking at least three years to get back to 2019 levels. Some regions will take even longer, with Asia Pacific potentially being one of the regions to recover faster.

In a (virtual) conference in Dallas last week, ACI World Economics Director Patrick Lucas presented a quasi-U-shaped / L-shaped recovery model. Despite the early and promising signs of capacity recovery, ACI is now looking at least three years to get back to 2019 levels. Some regions will take even longer, with Asia Pacific potentially being one of the regions to recover faster.

Source: ACI

Year to date, we see the same trend. The stock exchanges are within striking distance of a full recovery. Although the mega caps, often software companies, have led the way, aviation companies are following at a steady pace. The rate of recoveries are still wide, ranging from Airports of Thailand lacking 11% to beat the year’s high to Corporacion America at 45.2% below its January performance.  At the same time, the world reported 819,008 new confirmed cases, up from 764,800 the previous week. The number of fatalities was 30,851 this week, up 1,918 compared to last week (28,933). Given the massive demonstrations in many of the larger cities around the world, one concern will be if these will lead to a flare up of new cases in the weeks to come.

At the same time, the world reported 819,008 new confirmed cases, up from 764,800 the previous week. The number of fatalities was 30,851 this week, up 1,918 compared to last week (28,933). Given the massive demonstrations in many of the larger cities around the world, one concern will be if these will lead to a flare up of new cases in the weeks to come.

June 1, 2020

Slow Capacity Increases Will Test Appetite for Summer Travel

By Frode Skulbru, Modalis Vancouver May has come and gone with a variation of positive and negative news. The aviation market slowly added more capacity during the month in an attempt of a controlled opening of some economies. At the same time, Latin America seems to be new pandemic hotspot, resulting in further closures and new cases. This week, lower South America posted a 92.2% decline in seat capacity compared to January 2020. Nearly sixty airlines are relaunching services with some 267,000 additional flights scheduled to operate this week representing a near 16% increase on last week through a combination of the returning carriers and some capacity growth. Total capacity is now some 66% below last year. Demand is the critical issue. Domestic China and parts of Europe are reporting growth in booking activity but cancellations on short notice may be expected if load factors do not materialize.  Source: ICAO Aviation Stocks are not Recovering as Fast as the Market May has been a month of a bit of wait-and-see. The grey bars in the graph below now represents a full month and are therefore better comparable to the previous months. We now have two months of data post the late March shock to the financial markets. One interesting observation is that the Asian assets that showed signs of the earliest recovery all had a set-back in May. This could be a sign that even if the economy has slowly opened and capacity is being added, the demand for air-travel remains very low. Being based in Latin America, LAN had the largest decline in May losing 64.4% of its share value after an April gain of 20.4%.

Source: ICAO Aviation Stocks are not Recovering as Fast as the Market May has been a month of a bit of wait-and-see. The grey bars in the graph below now represents a full month and are therefore better comparable to the previous months. We now have two months of data post the late March shock to the financial markets. One interesting observation is that the Asian assets that showed signs of the earliest recovery all had a set-back in May. This could be a sign that even if the economy has slowly opened and capacity is being added, the demand for air-travel remains very low. Being based in Latin America, LAN had the largest decline in May losing 64.4% of its share value after an April gain of 20.4%.  Looking at year to date data, all assets remain below their values at New Years. All stock exchanges are on the road to recovery (so far), but of the airport stocks Beijing has lost further ground, Sydney remains unchanged. Qantas seem to be the airline on the fastest route to a share value recovery, adding 11% in value during May. Thai Airways posted a larger improvement, but the carrier was struggling on the brink of bankruptcy a couple of weeks ago only to be brought back by its majority owner, the Thai Government. In spite of massive gains on Wall Street (Facebook is now worth more than ever), Delta Airlines lost further value in May, sliding to 55.7% YTD.

Looking at year to date data, all assets remain below their values at New Years. All stock exchanges are on the road to recovery (so far), but of the airport stocks Beijing has lost further ground, Sydney remains unchanged. Qantas seem to be the airline on the fastest route to a share value recovery, adding 11% in value during May. Thai Airways posted a larger improvement, but the carrier was struggling on the brink of bankruptcy a couple of weeks ago only to be brought back by its majority owner, the Thai Government. In spite of massive gains on Wall Street (Facebook is now worth more than ever), Delta Airlines lost further value in May, sliding to 55.7% YTD.  Governments Continue to Offer Financial Support to Airlines Airlines have received $123 billion globally through several forms of financial aid from governments to get through the worst of the crisis. However, this has added to the industry’s debt – now approaching $550 billion. IATA states as the crisis deepens and recovery is now expected to take an extended period of time, governments should favor financial aid packages that raise equity rather than debt and set up airlines for a quicker recovery. So far, loand and loan guarantees constitutes half the support to date.

Governments Continue to Offer Financial Support to Airlines Airlines have received $123 billion globally through several forms of financial aid from governments to get through the worst of the crisis. However, this has added to the industry’s debt – now approaching $550 billion. IATA states as the crisis deepens and recovery is now expected to take an extended period of time, governments should favor financial aid packages that raise equity rather than debt and set up airlines for a quicker recovery. So far, loand and loan guarantees constitutes half the support to date.  Source: IATA According to ACI, “the contribution made by the aviation industry to global economic prosperity includes 65.5 million jobs around the world, including 10.5 million people employed at airports and by airlines, and supports $2.7 trillion in world economic activity”. Getting the aviation business back on its feet will therefore be key to a global economic recovery. Adding capacity is a first step, but the real question is if the public is confident enough in the early recovery to start traveling again in meaningful numbers? At the same time, the world reported 764,800 new confirmed cases, up from 689,000 the previous week. The number of fatalities was 28,933 this week, up 1,334 compared to last week (27,599). Both new cases and fatalities are increasing again, illustrating that all regions of the world are still not in sync as the pandemic continues to spread globally.

Source: IATA According to ACI, “the contribution made by the aviation industry to global economic prosperity includes 65.5 million jobs around the world, including 10.5 million people employed at airports and by airlines, and supports $2.7 trillion in world economic activity”. Getting the aviation business back on its feet will therefore be key to a global economic recovery. Adding capacity is a first step, but the real question is if the public is confident enough in the early recovery to start traveling again in meaningful numbers? At the same time, the world reported 764,800 new confirmed cases, up from 689,000 the previous week. The number of fatalities was 28,933 this week, up 1,334 compared to last week (27,599). Both new cases and fatalities are increasing again, illustrating that all regions of the world are still not in sync as the pandemic continues to spread globally.

May 25, 2020

Capacity is Holding Steady, but too Early to Gauge Demand as Countries are Slowly Easing Restrictions

In the tenth version of this series of articles, we see a flattening of the curve related to recovered seat capacity. Overall, there was a 1% decline for the week, however some countries are pulling back again. Italy had 8.2% less seats in the air compared to the previous week. India grounded over 20% more compared to the week before, due to a last minute extension of the lockdown for a further two weeks (note that the percentages are compared to the same week in 2019, hence do not reflect a direct change calculated from last week. If 2019 saw an increase this particular week and a similar increase did not occur this week, it will show as a negative on the graph below).  Where March was a month of great decline, April of some recovery, May has overall been relatively modest for the exchanges with single digit growth for all with the exception of HKEX in Hong Kong that has lost 2.8% so far in May.

Where March was a month of great decline, April of some recovery, May has overall been relatively modest for the exchanges with single digit growth for all with the exception of HKEX in Hong Kong that has lost 2.8% so far in May.  Thai Airways in the News Again Loss-making Thai Airways has been allowed to restructure its debts to keep its planes in the sky. The struggling airline had previously asked for a government bail-out via a $1.81 billion government guaranteed loan backed by the finance ministry which drove its share price up to $7.45 at the end of April, higher than at the start of the year. Today the stock was priced at $4.34. After a cabinet meeting on Tuesday, Thailand’s Prime Minister, Prayuth Chan-ocha, said: “The government has reviewed all dimensions… we have decided to petition for restructuring and not let Thai Airways go bankrupt. The airline will continue to operate.” China Eastern Losing Value Overall, China has been the country ahead of the curve compared to COVID-19 cases and economic activity compared to the rest of the world. Chinese carriers have added capacity for weeks, however China Eastern has now lost 16.1% of its value the last twenty days. Singapore Airlines is also down (38.4%) this month. Airports with Mixed Results Our airport sample have seen some mixed developments this month. Fraport is the winner so far with an 13.4% increase in May. ASUR, Airports of Thailand and Beijing are all down three weeks into the month.

Thai Airways in the News Again Loss-making Thai Airways has been allowed to restructure its debts to keep its planes in the sky. The struggling airline had previously asked for a government bail-out via a $1.81 billion government guaranteed loan backed by the finance ministry which drove its share price up to $7.45 at the end of April, higher than at the start of the year. Today the stock was priced at $4.34. After a cabinet meeting on Tuesday, Thailand’s Prime Minister, Prayuth Chan-ocha, said: “The government has reviewed all dimensions… we have decided to petition for restructuring and not let Thai Airways go bankrupt. The airline will continue to operate.” China Eastern Losing Value Overall, China has been the country ahead of the curve compared to COVID-19 cases and economic activity compared to the rest of the world. Chinese carriers have added capacity for weeks, however China Eastern has now lost 16.1% of its value the last twenty days. Singapore Airlines is also down (38.4%) this month. Airports with Mixed Results Our airport sample have seen some mixed developments this month. Fraport is the winner so far with an 13.4% increase in May. ASUR, Airports of Thailand and Beijing are all down three weeks into the month.  Year to Date Results Still Depressed After earlier improvements, five of seven airlines now have a lower market cap than at the end of March. Any gains from the hope of a V shaped recovery modelled on China’s apparent three-month closure and backed by trillions of dollars in government sponsored aid seem to have been partially lost. LAN is the worst off of the airlines, not surprising as Latin America seems to be one of the hot spots of the pandemic these days. As for airport values, Sydney and Beijing remain around 30% below the start of 2020. Followed by Fraport (-44.4%) and ASUR (-48.0%). Corporacion America rounds it off at -60.6%. Airports of Thailand remain the most improved at 22.9% below January 2nd, however with its main carrier now facing more difficulties we may see some changes in the weeks to come. At the same time, the world reported 689,000 new confirmed cases, slightly up from 652,000 the previous week. The number of fatalities was 27,599 this week, down 5,985 compared to last week (33,584).

Year to Date Results Still Depressed After earlier improvements, five of seven airlines now have a lower market cap than at the end of March. Any gains from the hope of a V shaped recovery modelled on China’s apparent three-month closure and backed by trillions of dollars in government sponsored aid seem to have been partially lost. LAN is the worst off of the airlines, not surprising as Latin America seems to be one of the hot spots of the pandemic these days. As for airport values, Sydney and Beijing remain around 30% below the start of 2020. Followed by Fraport (-44.4%) and ASUR (-48.0%). Corporacion America rounds it off at -60.6%. Airports of Thailand remain the most improved at 22.9% below January 2nd, however with its main carrier now facing more difficulties we may see some changes in the weeks to come. At the same time, the world reported 689,000 new confirmed cases, slightly up from 652,000 the previous week. The number of fatalities was 27,599 this week, down 5,985 compared to last week (33,584).

May 18, 2020

Early Positive Signs of Government Support followed by a Slow Re-opening of the Economy Seems to be Wearing Off as Five of Six Airport Reference Stocks Lose Ground

In the ninth version of this series of articles, the German assets are the best performers. Both Fraport (7.6%) and Lufthansa (2.8%) gained value last week, likely on the back of a slow but directed opening off the German economy. The largest loss of values this week was experienced by Asian assets. Thai Airways, one that previously outperformed its own January value in the middle of the pandemic, declined 44.2% last week. This dragged Airports of Thailand with it, resulting in a 6.0% drop since last Monday. Both Chinese and Australian assets saw a set back as illustrated in the graph below.  On a year-to-date basis, five assets remain below 50% of its January value. In Latin America, LAN remains at 71.4% below, followed by Corporacion America at 63.9%. Santiago was again under complete lock-down from Friday May 15th, likely contributing to the bleak situation (LAN closed at $2.76 on Friday before recovering somewhat today). In Asia, Qantas (-55.8%) and Singapore Airlines (-61.6%) both show a similar pattern. The three assets with the most improved recovery so far are all airports; Airports of Thailand are 22.3% below its January value, followed by Beijing (-29.7%) and Sydney (-34.8%).

On a year-to-date basis, five assets remain below 50% of its January value. In Latin America, LAN remains at 71.4% below, followed by Corporacion America at 63.9%. Santiago was again under complete lock-down from Friday May 15th, likely contributing to the bleak situation (LAN closed at $2.76 on Friday before recovering somewhat today). In Asia, Qantas (-55.8%) and Singapore Airlines (-61.6%) both show a similar pattern. The three assets with the most improved recovery so far are all airports; Airports of Thailand are 22.3% below its January value, followed by Beijing (-29.7%) and Sydney (-34.8%).

The Infamous Middle Seat

The Infamous Middle Seat

Much has been written about (hopefully) temporary measures that have been and will be put in place as airports and airlines vie for customers to return. This range from distancing at airports, use of face masks, cleaning protocols and empty middle seats. On average, the airlines managed to fill around 85% of seats in 2019. Anyone in the industry understands that this will not be possible with all middles seats un-occupied. The most positive news from last week is the continuous increase of capacity in various markets.  Source: OAG OAG reports we have broken through the 30 million weekly seat mark. 83 million seats are still missing from the (old) normal flight capacity, but the signs of recovery are there with two weeks of consistent growth. Compared to the same week last year, we are now 73% lower. This reflects the total capacity, but now back to the middle seat issue. Florida Panhandle has presented some high-level profit calculations based on a set of assumptions and load factors for the four largest U.S. carriers. At the 2019 target load factor of 85%, all four carriers made a profit, with Southwest and Delta the best performers at $4,700 followed by United at $3,700 and American at $2,600. The same model calculates a break-even load factor in the low to high seventies.

Source: OAG OAG reports we have broken through the 30 million weekly seat mark. 83 million seats are still missing from the (old) normal flight capacity, but the signs of recovery are there with two weeks of consistent growth. Compared to the same week last year, we are now 73% lower. This reflects the total capacity, but now back to the middle seat issue. Florida Panhandle has presented some high-level profit calculations based on a set of assumptions and load factors for the four largest U.S. carriers. At the 2019 target load factor of 85%, all four carriers made a profit, with Southwest and Delta the best performers at $4,700 followed by United at $3,700 and American at $2,600. The same model calculates a break-even load factor in the low to high seventies.  Removing the sale of all middle seats will reduce the potential load factor to about 66%. In the early days of recovery, the empty middle seat may not make a difference as the demand may not be sufficiently high to fill all seats (or at least 85%), however in the longer run, an empty middle seat would not be sustainable with todays fares. Using the same assumptions as listed below, each carrier will lose money on such flights. Southwest will likely be “best” off with a loss of $2,600, followed by Delta ($3,400), United ($3,700) and American ($5,200).

Removing the sale of all middle seats will reduce the potential load factor to about 66%. In the early days of recovery, the empty middle seat may not make a difference as the demand may not be sufficiently high to fill all seats (or at least 85%), however in the longer run, an empty middle seat would not be sustainable with todays fares. Using the same assumptions as listed below, each carrier will lose money on such flights. Southwest will likely be “best” off with a loss of $2,600, followed by Delta ($3,400), United ($3,700) and American ($5,200).  Source: Florida Panhandle Assumptions: Utilizing public information in SEC annual filings, the data team has approximated the cost of operating a 216-passenger flight on a 1,000-mile route. The simulated flight represents an average for the airline system-wide and factors industry standard reporting metrics including CASM (Cost Per Available Seat Mile) and TRASM (Total Revenue Per Available Seat Mile) to reach the conclusions presented above. The actual cost to operate a given flight may differ based on market changes or route-specific factors. At the same time, the world reported 652,000 new confirmed cases, slightly up from 607,000 the previous week. The number of fatalities was 33,584 this week, down 1,283 compared to last week (34,867).

Source: Florida Panhandle Assumptions: Utilizing public information in SEC annual filings, the data team has approximated the cost of operating a 216-passenger flight on a 1,000-mile route. The simulated flight represents an average for the airline system-wide and factors industry standard reporting metrics including CASM (Cost Per Available Seat Mile) and TRASM (Total Revenue Per Available Seat Mile) to reach the conclusions presented above. The actual cost to operate a given flight may differ based on market changes or route-specific factors. At the same time, the world reported 652,000 new confirmed cases, slightly up from 607,000 the previous week. The number of fatalities was 33,584 this week, down 1,283 compared to last week (34,867).

May 11, 2020

Aviation Industry in Holding Pattern as Capacity Increases Slightly while Markets Await Q1 & Q2 Real Impact

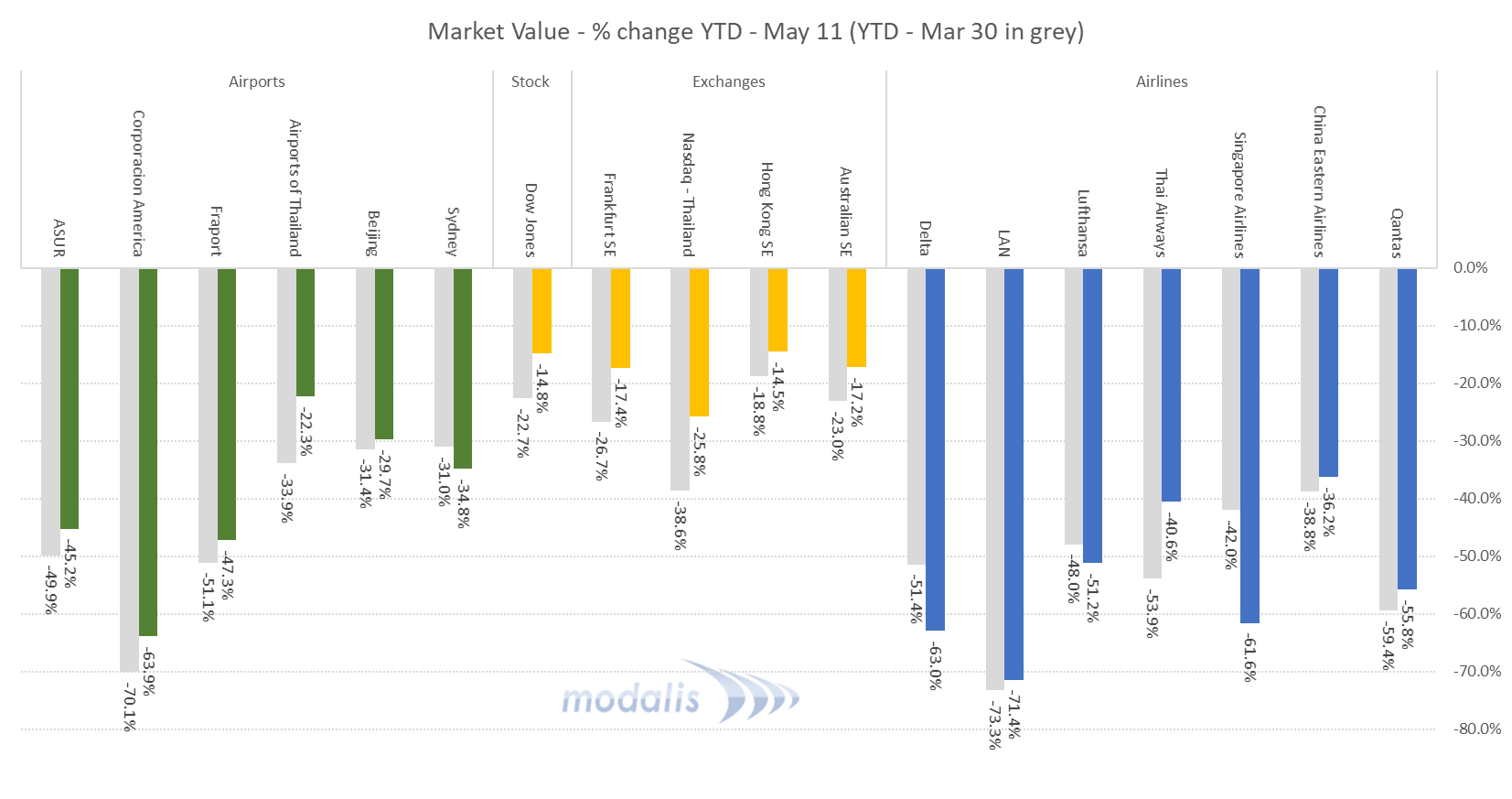

In the eight version of this series of articles, the aviation industry seems to have entered a holding pattern from a valuation point of view. Four of the six airport companies included in the analysis lost ground last week as did all seven airlines. In the meantime, the overall indexes keep gaining value. This is on the back of a 600,000 capacity gain last week, resulting in total worldwide capacity of 29.9 million seats, some 80 million less than a year ago. Next weeks projections are at 42.3 million according to the latest numbers from OAG.  The following table includes weekly (Mondays) value of the select assets. The decline of the airline values this week is likely and partially linked to the newly released information about travel limitations at airports and in-flight (empty middle seats etc.) which will limit load factors and corresponding revenue generation. We may also see the first real financial impact on some carriers in the weeks to come if the government support is in-sufficient. For example, Avianca filed for Chapter 11 bankruptcy in the US Southern District of New York on Sunday, blaming its collapse on the “unforeseeable impact of the Covid-19 pandemic,” according to a company statement. Last month, Virgin Australia collapsed after failing to obtain a government bailout. In March, UK budget carrier Flybe entered administarrtion, saying its financial challenges were too great to withstand in the context of the pandemic.

The following table includes weekly (Mondays) value of the select assets. The decline of the airline values this week is likely and partially linked to the newly released information about travel limitations at airports and in-flight (empty middle seats etc.) which will limit load factors and corresponding revenue generation. We may also see the first real financial impact on some carriers in the weeks to come if the government support is in-sufficient. For example, Avianca filed for Chapter 11 bankruptcy in the US Southern District of New York on Sunday, blaming its collapse on the “unforeseeable impact of the Covid-19 pandemic,” according to a company statement. Last month, Virgin Australia collapsed after failing to obtain a government bailout. In March, UK budget carrier Flybe entered administarrtion, saying its financial challenges were too great to withstand in the context of the pandemic.  Year to date, the industry is still in deep discount territory. Thai Airways has had a positive development the last few weeks are now back in negative territory.

Year to date, the industry is still in deep discount territory. Thai Airways has had a positive development the last few weeks are now back in negative territory.  Both airlines and airports continue to fortify their financial position through more debt, share issues and/or Government support. In the U.S. all four major carriers have raised substantial capital:

Both airlines and airports continue to fortify their financial position through more debt, share issues and/or Government support. In the U.S. all four major carriers have raised substantial capital:

- American Airlines: USD4.18 billion in direct relief + USD1.78 billion in low interest loans. AA is eligible for another USD4.75 billion long term loan.

- Delta Airlines: USD3.8 billion in direct relief + USD1.6 billion in low interest loans. Delta eligible for another USD4.6 billion long term loan. Other financing includes USD3.0 billion term loan and USD1.2 billion aircraft sale and lease back.

- United Airlines: USD3.5 billion in direct relief + USD1.5 billion in low interest loans. UA is eligible for another USD4.5 billion long term loan. Other financing includes USD1.0 billion of equity, and an un-disclosed sum based on an aircraft sale and lease back agreement with BOC Aviation. A further USD2.25 billion through a bond offering is planned.

- Southwest Airlines: USD2.3 billion in direct relief + USD0.948 billion in low interest loans. Other financing includes a USD1.6 billion planned equity issuance, and USD1.0 billion in senior convertible notes.

In the meantime, the world reported 607,000 new confirmed cases, slightly up from the increase the previous two weeks. The number of fatalities was 34,867, down from 40,449 last week and 41,122 two weeks ago.

May 4, 2020

Global Capacity Continues to Decrease, but Some Markets are Slowly Turning the Tide

This is the seventh week of this series of articles where we track a select number of aviation assets through the pandemic and corresponding financial downturn. As a reminder, the map below shows the location of the assets in question.  According to OAG, global capacity of scheduled flights is now down by 70% compared to the same week last year. This is the lowest since the start of the crisis. Many countries continue to maintain restrictions on air passenger arrivals, leading airlines to continue removing capacity from their schedules including the US which again reduced capacity last week (11% reduction to a total of 74.5% compared to early May 2019).

According to OAG, global capacity of scheduled flights is now down by 70% compared to the same week last year. This is the lowest since the start of the crisis. Many countries continue to maintain restrictions on air passenger arrivals, leading airlines to continue removing capacity from their schedules including the US which again reduced capacity last week (11% reduction to a total of 74.5% compared to early May 2019).  Source: OAG Elsewhere, many countries appear to be have slightly more flights operating than a week ago and the year-over-year flight volumes are slowly improving. As for stock prices, April was a month of recovery as five of the six airport companies posted a positive development in share value for April, the only exception being Sydney that had a modest (in these times) 2.9% decline.

Source: OAG Elsewhere, many countries appear to be have slightly more flights operating than a week ago and the year-over-year flight volumes are slowly improving. As for stock prices, April was a month of recovery as five of the six airport companies posted a positive development in share value for April, the only exception being Sydney that had a modest (in these times) 2.9% decline.  All stock markets in the survey saw recoveries as did most airlines except Lufthansa (- 8.8%) and Delta (- 21.3%). The clear winner is again Thai Airways that has gone from a share price of $2.78 the week of March 23 to $7.35 today (recall that the airline is 51% owned by the State and has received substantial subsidies). The following graph shows the development the first four months of the year and illustrates the same development.

All stock markets in the survey saw recoveries as did most airlines except Lufthansa (- 8.8%) and Delta (- 21.3%). The clear winner is again Thai Airways that has gone from a share price of $2.78 the week of March 23 to $7.35 today (recall that the airline is 51% owned by the State and has received substantial subsidies). The following graph shows the development the first four months of the year and illustrates the same development.  Given the above indication of a slow capacity increase the coming weeks and the news that more countries are now starting to ease general restrictions and lockdowns, we may at this stage be entering into a new phase where a new (hopefully temporary) reality may apply. Several countries have indicated measures at airports that will need to be in place before travel volumes can increase and today Air Canada released its new “CleanCare+” program where the carrier takes the initiative to impose somewhat strict measures on each passenger before any is allowed on board. Air Canada states this is a comprehensive program to provide greater peace of mind during all stages of travel and includes:

Given the above indication of a slow capacity increase the coming weeks and the news that more countries are now starting to ease general restrictions and lockdowns, we may at this stage be entering into a new phase where a new (hopefully temporary) reality may apply. Several countries have indicated measures at airports that will need to be in place before travel volumes can increase and today Air Canada released its new “CleanCare+” program where the carrier takes the initiative to impose somewhat strict measures on each passenger before any is allowed on board. Air Canada states this is a comprehensive program to provide greater peace of mind during all stages of travel and includes:

- Mandatory pre-flight customer temperature checks, the first in the Americas

- More personal space in Economy Class at least until June 30, 2020 (i.e. empty middle seats)

- Personal care kits containing disinfectant and safety items

- Electrostatic cabin spraying to reinforce aircraft grooming protocols

- Revised food product minimizing crew and passenger contact

- Customer face-coverings and employee Personal Protective Equipment now mandatory at all times

In addition, the already in place procedures continue:

- Protocols for the use of Personal Protective Equipment by employees, including face shields and coverings, gloves and gowns by in-flight crew.

- Revised check-in procedures to allow for all government entry requirements, mandatory health questionnaire and other relevant information to be entered on-line or at check-in kiosks.

- Temporary adjustments to on-board service such as individual water bottles instead of bar service offerings and the removal of pillows and blankets; empty seat back pockets.

- Use of a third-party company that monitors infectious diseases all over the world using Artificial Intelligence and other predictive tools to improve reporting and reduce decision times.

- No change or cancellation fee for existing or new bookings.

Air Canada is also working with airports on additional protective and sanitary measures. Similar measures have been communicated in various parts of the world. These will of course be added on top of the regular security protocols. Michael O’Leary of Ryanair fame stated some weeks ago that Ryanair would not commence flying if there is a requirement to keep middle seats empty unless Governments would be willing to pay for the same. It remains to be seen how passengers respond to all of this when it comes time to fly! In the meantime, the world reported 580,000 new confirmed cases, about the same increase as the previous two weeks. The number of fatalities was 40,449 last week, down from 41,122 the week before and 50,242 three weeks ago.

April 27, 2020

Early Signs of Value Recovery Coincides with Capacity Hitting Rock Bottom Five of the six airport companies included in our study had a positive development last week. Corporacion America was the big winner in April, having recovered 27.1% during the last four week, albeit from a low base. Sydney was the only airport that continue to lose value ending at minus 2.5% for April. The broader and corresponding stock markets all showed signs of improvements during April, recovering from the shock in late March. We will follow these with great interest as the initial stimulus packages are rolled out and early reports of un-employment and corporate projections are being released in May. As for the airlines, Lufthansa (-8.6%) and Delta (-22.7%) were the only two that continue to lose ground the last seven days and for April as a whole. The Financial Times announced that Delta plans to raise additional debt in an attempt to bring its total liquidity up to $10 billion by the end of the current quarter, up from $6 billion on March 31. Delta is seeing such strong demand for its debt that the airline has increased a planned $3 billion offering by an additional $2 billion. Airlines and their investors for now are hoping that as the pandemic is contained, traffic will at least turn to more normalized recessionary levels. Delta nevertheless expects second quarter revenues to fall 90% year-over-year. There is a view that it is likely going to take three years, if not longer, for travel demand to return to pre-pandemic levels.  On a year to date basis, Thai Airways is the only one with increased value four months into 2020 (see last week’s article for further details). Delta and Lufthansa are the sole two that lost additional value during the month of April, with Delta now posting a 62.5% decline so far this year. On a positive note, OAG reports that scheduled airline capacity has increased for the first time in nearly ten weeks and perhaps reassuringly in more than one market. With some countries beginning to ease lockdown restrictions, a few airlines are cautiously testing market demand with some capacity being added back. This week’s adjusted scheduled capacity, whilst still below 30 million seats, represents a 2% recovery on last weeks adjusted volumes.

On a year to date basis, Thai Airways is the only one with increased value four months into 2020 (see last week’s article for further details). Delta and Lufthansa are the sole two that lost additional value during the month of April, with Delta now posting a 62.5% decline so far this year. On a positive note, OAG reports that scheduled airline capacity has increased for the first time in nearly ten weeks and perhaps reassuringly in more than one market. With some countries beginning to ease lockdown restrictions, a few airlines are cautiously testing market demand with some capacity being added back. This week’s adjusted scheduled capacity, whilst still below 30 million seats, represents a 2% recovery on last weeks adjusted volumes.  On the airport side, the first quarter decline has stabilized and five of the six companies have a slightly improved enterprise value as we head into the fifth month of the year.

On the airport side, the first quarter decline has stabilized and five of the six companies have a slightly improved enterprise value as we head into the fifth month of the year.

April 20, 2020

Reduced volatility, signs of recovery as sovereign support takes effect! All six airport stocks included in the below graph had a positive development last week. Airports of Thailand continue to lead the pack with a 24.6% appreciation after April 13 (see further comments below). The broader and corresponding stock markets show similar positive results for the week. As for the airlines, Lufthansa (-3.7%) and Delta (-17.5%) were the only two that lost ground the last seven days. Delta’s share price is tightly linked to the anticipated $29 billion rescue package, and its value has likely declined due to a delay in payouts and requests for further information and details from the U.S. Treasury. Although the law (for support) was signed March 27th and were planned to be paid ten days after, the Treasury has been given discretion related to the timing.  Thai Airways are now worth more than it was at the beginning of 2020 Thailand expects liquidity support for Thai Airways this week, it was reported last Thursday. Share prices rose after the comments and the 51% state owned carrier is now worth 8% more than at the beginning of 2020 – without flying as Thai Airways suspended its flights last month. Thailand last week extended a ban on passenger flights until the end of April to limit the spread of the coronavirus. The country has a total of 2,672 cases and 46 fatalities. This illustrates the impact of the Government stimulus in Thailand and likely in many other countries. A key question to ask would be if this is sufficient or will even the deep coffers of Governments eventually be empty if the pandemic continues over additional months? Thai Airways was already facing financial trouble, reporting losses since 2017. Losses in 2019 widened to 12.2 billion baht ($385 million) from losses of 11.6 billion baht a year earlier.

Thai Airways are now worth more than it was at the beginning of 2020 Thailand expects liquidity support for Thai Airways this week, it was reported last Thursday. Share prices rose after the comments and the 51% state owned carrier is now worth 8% more than at the beginning of 2020 – without flying as Thai Airways suspended its flights last month. Thailand last week extended a ban on passenger flights until the end of April to limit the spread of the coronavirus. The country has a total of 2,672 cases and 46 fatalities. This illustrates the impact of the Government stimulus in Thailand and likely in many other countries. A key question to ask would be if this is sufficient or will even the deep coffers of Governments eventually be empty if the pandemic continues over additional months? Thai Airways was already facing financial trouble, reporting losses since 2017. Losses in 2019 widened to 12.2 billion baht ($385 million) from losses of 11.6 billion baht a year earlier.  Naturally, Airports of Thailand sees an up-tick in value, albeit not to the same extent. The central and south American airport operators remain at the other end of the spectrum although with a slight improvement so far this month.

Naturally, Airports of Thailand sees an up-tick in value, albeit not to the same extent. The central and south American airport operators remain at the other end of the spectrum although with a slight improvement so far this month.

April 13, 2020

Have we reached the bottom or is this another bear market rally? The Easter week presented a good outcome for most of the stocks tracked in this article series. As illustrated in the graph below, Delta airlines is the only airline stock that did not have a positive development so far this month. All the exchanges have re-gained ground since March 31st, with three of the six airports also ending in positive territory – Airports of Thailand being the clear frontrunner at 12.1%, riding on the 74.5% gain of Thai Airways.  Weekly capacity reductions slowed last week as many regional markets now appear to have reached a point where less than 15% of historic capacity is being operated. Western Europe, the Southwest Pacific and Lower South America are all reporting capacity some 90% below the levels planned in the week of the 20th January. North East Asia at a regional level has a 1% increase in capacity week on week (Source: OAG).

Weekly capacity reductions slowed last week as many regional markets now appear to have reached a point where less than 15% of historic capacity is being operated. Western Europe, the Southwest Pacific and Lower South America are all reporting capacity some 90% below the levels planned in the week of the 20th January. North East Asia at a regional level has a 1% increase in capacity week on week (Source: OAG).  Overall, a similar pattern emerges. ASUR (-1.8%), Sydney Airport (-4.7%), Corporacion America (-1.1%) and Delta (-18.9%) all lost additional ground last week. All remaining assets gained some ground last week with Thai Airways leading the pack, now at a 19.6% decline so far this year. At the same time, the number of confirmed cases of COVID-19 increased to 1.93 million cases, a 44% increase from the week before, with fatalities being reported at 119,701, a 61% increase from the week before. While the percentage increase is reducing, the absolute cases from last week increased from 561K to 588k (the percentage increase would naturally drop as the total gets larger). Unfortunately, the same is the case of the number of deaths, increasing from 37k to 45k.

Overall, a similar pattern emerges. ASUR (-1.8%), Sydney Airport (-4.7%), Corporacion America (-1.1%) and Delta (-18.9%) all lost additional ground last week. All remaining assets gained some ground last week with Thai Airways leading the pack, now at a 19.6% decline so far this year. At the same time, the number of confirmed cases of COVID-19 increased to 1.93 million cases, a 44% increase from the week before, with fatalities being reported at 119,701, a 61% increase from the week before. While the percentage increase is reducing, the absolute cases from last week increased from 561K to 588k (the percentage increase would naturally drop as the total gets larger). Unfortunately, the same is the case of the number of deaths, increasing from 37k to 45k.

April 6, 2020

Stock Markets Rebound Slightly as Aviation Stocks Continue to Trade in Negative Territory (with two notable exceptions) The week from March 30 to April 6 resulted in a further decline of 11 of 13 aviation stocks in this overview despite a small recovery of the corresponding stock exchanges. Notable exceptions were Fraport and Thai Airways that recovered by 10.1% and 15.7% respectively. The decline is likely a result related to the news that globally airlines removed a further 11.1 million seats from the OAG database this week, equivalent to a 22.7% reduction week on week.  Weekly capacity is now just above one-third of that originally scheduled for this week and with further cuts being advised by airlines through to the end of May we should expect more capacity cuts next week (Source: OAG).

Weekly capacity is now just above one-third of that originally scheduled for this week and with further cuts being advised by airlines through to the end of May we should expect more capacity cuts next week (Source: OAG).  Year to date, a similar pattern emerges. Thai Airways is the only airline of the seven reported here that maintained the positive position from last week. Fraport shows the same trend on the airport side. At the same time, the number of confirmed cases of COVID-19 increased to 1.4 million, a 72% increase from the week before.

Year to date, a similar pattern emerges. Thai Airways is the only airline of the seven reported here that maintained the positive position from last week. Fraport shows the same trend on the airport side. At the same time, the number of confirmed cases of COVID-19 increased to 1.4 million, a 72% increase from the week before.

March 30, 2020

Aviation Sector Receives a Boost as Stock Markets Rally on the Back of Announced Stimulus Packages The week from March 23 to March 30 saw a recovery of our select aviation assets as the world’s markets improved, to a large extent on the back of the various Government announced stimulus packages.  These are good news however several large-scale capacity reductions last week may continue to impact the market in the days to come. These include among others Ryanair’s decision to ground all flights until June, severe reductions by Qantas, Etihad and Emirates, the closing of borders in Thailand and India’s decision to cease all domestic flights for the time being.

These are good news however several large-scale capacity reductions last week may continue to impact the market in the days to come. These include among others Ryanair’s decision to ground all flights until June, severe reductions by Qantas, Etihad and Emirates, the closing of borders in Thailand and India’s decision to cease all domestic flights for the time being.  Overall, a similar pattern emerges. While still in solid negative territory since the beginning of 2020, every asset has started a claw-back based on last weeks results. At the same time, the number of confirmed cases of COVID-19 doubled again, now to over three quarter million CONFIRMED cases.

Overall, a similar pattern emerges. While still in solid negative territory since the beginning of 2020, every asset has started a claw-back based on last weeks results. At the same time, the number of confirmed cases of COVID-19 doubled again, now to over three quarter million CONFIRMED cases.

March 23, 2020

The aviation sector values continue to decline amidst a doubling of confirmed COVID-19 cases The week from March 16 to March 23 saw a continuous overall decline of our select aviation assets. A notable exception are the German companies where both Lufthansa (0.3%) and Fraport (6.9%) increased in value the last seven days on the back of a flat result at the Frankfurt Stock Exchange. Sydney Airport also posted an improvement of 4.4%.  Year to date, the overall decline continues, now with three assets posting YTD declines of over 70%. Strangely enough, among the airport companies in this overview, Beijing is the one with the lowest decline in value.

Year to date, the overall decline continues, now with three assets posting YTD declines of over 70%. Strangely enough, among the airport companies in this overview, Beijing is the one with the lowest decline in value.  At the same time, OAG reports a 23% capacity reduction in one week that leaves us with some 37 million fewer seats than some ten weeks ago; some 35% of capacity has been wiped out and more is likely to follow in the coming weeks as airlines continually adjust their schedules. A glimmer of hope comes from China where an addition of a further 217,000 domestic seats could be seen as positive against what is a dramatic situation.

At the same time, OAG reports a 23% capacity reduction in one week that leaves us with some 37 million fewer seats than some ten weeks ago; some 35% of capacity has been wiped out and more is likely to follow in the coming weeks as airlines continually adjust their schedules. A glimmer of hope comes from China where an addition of a further 217,000 domestic seats could be seen as positive against what is a dramatic situation.

March 16, 2020

The world’s stock markets have taken a beating the last few weeks. Businesses around the world are impacted as investors are exiting the market and consumers are being more cautious. Airports are no exception as the volume of travellers are dwindling, airlines are reducing seat capacity and borders are closing. With multiple revenue sources and the ability to attract new carriers if one exits, airports have traditionally been more resilient to economic fluctuations than airlines, but not in this market. Modalis IR has compiled data from a select group of traded airports, airlines and the stock exchanges these are traded on to investigate how the economic fall-out from the COVID-19 has made an impact. The first graph below shows the percentage change in value for Jan, Feb and the first two weeks of March 2020. While January saw a decline (blue bars), it could be seen as a correction after record highs leading up to the new year. There are even some positive results this month. The value of the airports in our selection declined on average 8.3% in January, compared to a 15.7% decline in airline stocks and an overall 3.9% decline of the exchanges included in this comparison. Confirmed COVID-19 cases at the end of January was limited to fifteen thousand and mostly in China.  In February (orange bars), it was clear the world was facing a major challenge. Confirmed cases hit over ninety thousand and had by then started spreading around the world. The sampe group of airlines were down 17.4% compared to 12.1% for the airports. The select exchanges were down 6.7%. The aviation industry has generally been pro-cyclical to the rest of the market. It drops earlier and faster but is also quick to recover when times are good. So is the case it seems this time as well. So far this month (March), the airports in this overview dropped 31.2% of their value experiencing the full impact of world-wide cases that have dragging most stock markets firmly into bear territory (grey bars above). The comparable stock exchanges lost 22.0% the same period with the airlines performing roughly the same at 23.0%. Note the notable exception of Thai Airways that actually gained 4.7% value so far in March (albeit after losing 50% in January and February). In total (Jan – Mar 16), we observe airport values (green bars) decline from 21.9% to 71.9% over two and a half months. As the number of virus cases are passing 180 thousand with most international travel being curtailed until we see a flattening and decline in new corona cases, it is difficult to imagine a recovery in the immediate future.

In February (orange bars), it was clear the world was facing a major challenge. Confirmed cases hit over ninety thousand and had by then started spreading around the world. The sampe group of airlines were down 17.4% compared to 12.1% for the airports. The select exchanges were down 6.7%. The aviation industry has generally been pro-cyclical to the rest of the market. It drops earlier and faster but is also quick to recover when times are good. So is the case it seems this time as well. So far this month (March), the airports in this overview dropped 31.2% of their value experiencing the full impact of world-wide cases that have dragging most stock markets firmly into bear territory (grey bars above). The comparable stock exchanges lost 22.0% the same period with the airlines performing roughly the same at 23.0%. Note the notable exception of Thai Airways that actually gained 4.7% value so far in March (albeit after losing 50% in January and February). In total (Jan – Mar 16), we observe airport values (green bars) decline from 21.9% to 71.9% over two and a half months. As the number of virus cases are passing 180 thousand with most international travel being curtailed until we see a flattening and decline in new corona cases, it is difficult to imagine a recovery in the immediate future.  The following table contains the data used in the above graphs:

The following table contains the data used in the above graphs: