Login/Register

Brazil’s Airport Privatizations: What you Need to Know About the 7th Round (Part 1 of 2)

André Soutelino

June 9, 2021

|

In the first of a two-part examination of Brazil’s 7th round of airport privatizations we look at the three clusters available and their component airports. In Part 2, we will discuss the pros and cons of each batch. |

Brazil has been privatizing its airports over an extended period since 2012 to speed up the process of transport infrastructure modernization. Among the 66 airports that were run by state-owned Empresa Brasileira de Infraestrutura Aeroportuária (Infraero), many have been snapped up after several rounds of sell-offs over the years, the latest of which we covered here.

After the 7th round, Infraero will effectively become more of a service provider, hired to manage airports as is the case now at five small gateways.

The first privatization round didn’t have any Infraero participation: it was to build and operate São Gonçalo do Amarante (NAT) which serves Natal. In rounds 2 and 3, Infraero partnered with new concessionaires using a Public-Private Partnership (PPP or P3) model where the state entity held onto a 49% stake.

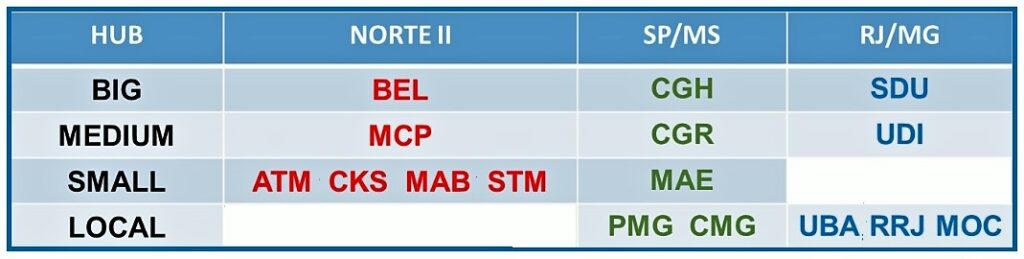

Seventh round airports are available in 3 clusters

The 4th round was the only one where single-airport concessions were granted: 30 years each for Salvador’s Deputado Luís Eduardo Magalhães International (SSA), Fortaleza-Pinto Martins International (FOR) and Florianópolis Hercílio Luz International, branded Floripa Airport (FLN); and 25 years for Salgado Filho International (POA) serving Porto Alegre.

From the 5th round onwards airports were offered in clusters – the so-called ‘steak with the bone’ model where a leading and usually profitable airport was batched up with some smaller less profitable or loss-making ones.

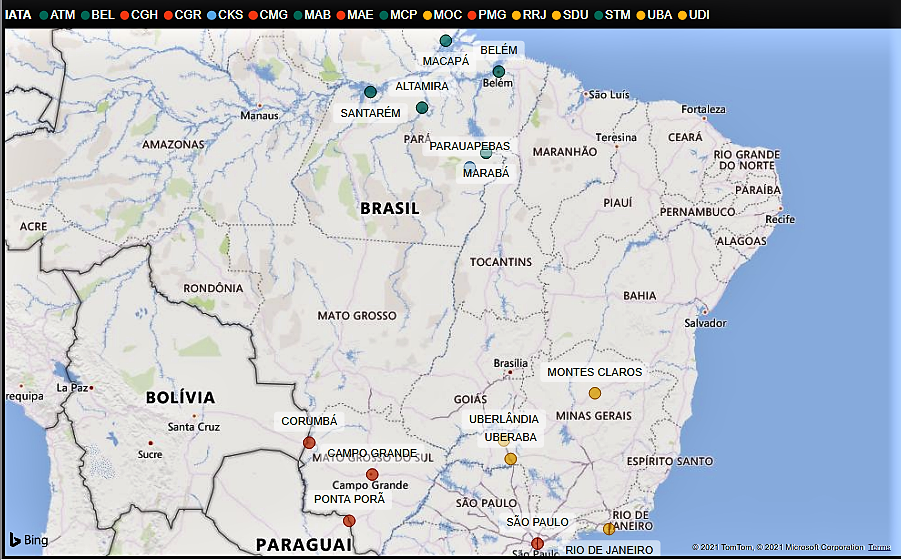

Where the 16 airports are located

What’s on Offer in Round 7?

In the 7th round the state will offer 16 airports divided into three clusters:

- Norte II

- SP/MS

- RJ/MG

The last remaining jewels in Brazil’s aviation crown – São Paulo’s Congonhas-Deputado Freitas Nobre Airport (CGH) and Rio de Janeiro’s Santos Dumont Airport (SDU) – are in this round. CGH is part of the SP/MS cluster and SDU part of RJ/MG.

According to Brazil’s air transport masterplan published in 2018, and following official airport classification (pre-COVID), the airports from the 7th round are designated as big, medium, small and local (see table).

The Norte II cluster is anchored by Belem

Cluster Norte II – Six airports where Belém (BEL) is the leading gateway and classified as big, and Macapá (MCP) listed as medium. This cluster has more small airports than the others, with five of them concentrated in Pará state in northern Brazil.

Cluster SP/MS – These five airports include the most valuable across the whole 7th round: São Paulo’s CGH. It will therefore be quite attractive, helped also by a former ban on commercial international flights at CGH being revoked. At MAE there is room to develop the business aviation segment. On the other hand, Ponta Porã International Airport (PMG) on the Paraguayan border has no regular routings at present.

The SP/MS cluster has an interesting mix of gateways

Cluster RJ/MG – Another batch of five, with the pulling power coming from Rio’s SDU. Jacarepaguá–Roberto Marinho (RRJ) a general aviation airport close to Rio is the second most valuable asset because offshore companies are headquartered in the area and they transport passengers to the Campos oil and gas basin. Uberlândia–Tenenete Coronel Aviador César Bombonato Airport (UDI), south of Brasilia, is larger and ranked as medium-sized.

Some of these smaller airports may seem limited in their value, but the COVID19 pandemic has been an opportunity for regional aviation. Airports classified as ‘medium’ and ‘local’, based on Civil Aviation Authority guidelines, have seen some boosts to their regular routes as more small planes, direct services and domestic tourism have all increased.

Brazil’s pandemic experience has shown that national traffic can recover fast. Besides, the Brazilian government has announced that it will deregulate the aviation sector by 2022 at the latest. This will allow for, among other things, commercial seaplane services, as well as give smaller gateways more scope to expand and develop new business.

Now is the time that the country can realistically look again to a future with a fully integrated air network, something that last existed in the 1960s and 1970s when the air transport market was a little more fragmented.

[Part 2 was published on June 16, 2021]

|

For a more detailed analysis of the 7th round we can offer the following:

For further information about this data, contact Modalis at [email protected] |