Login/Register

Airline Recovery in Europe Led by Ryanair

Dion Zumbrink

October 25, 2023

© Piotr Mitelski / Ryanair

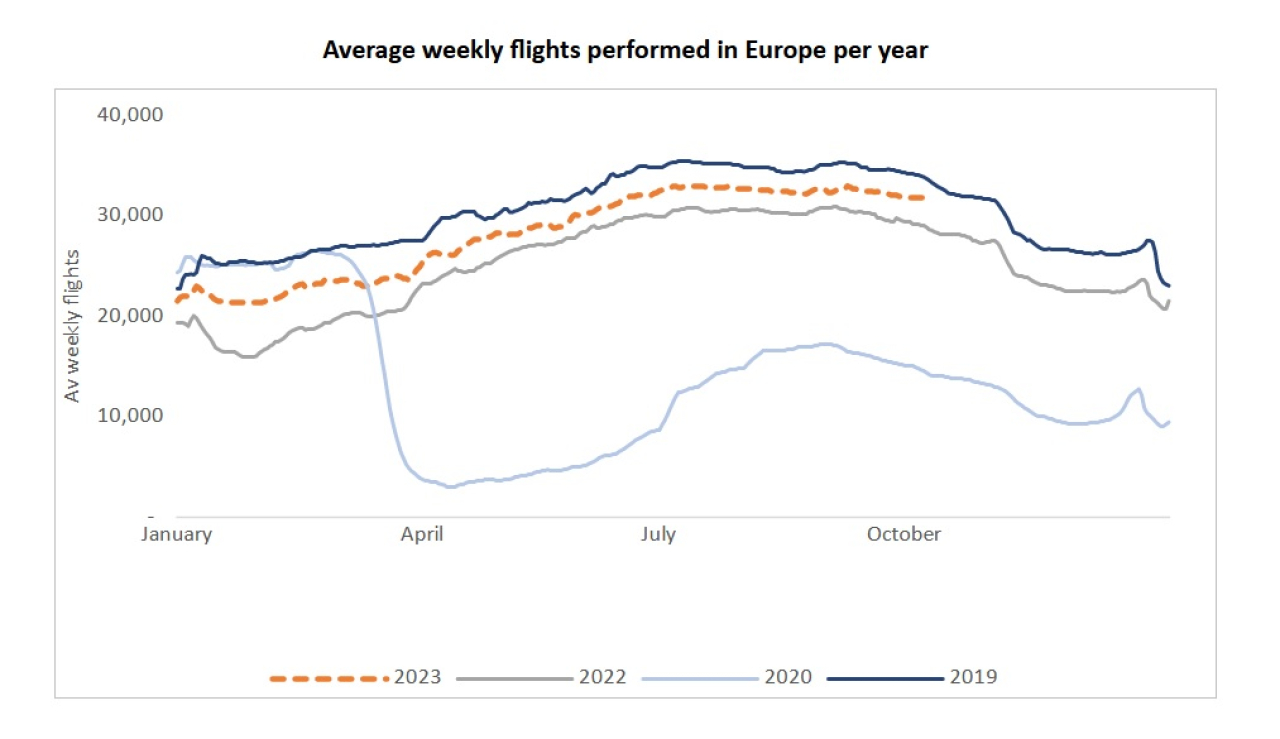

With the 2023 summer season in Europe drawing to a close, we can take a look at the performance of the airlines in this market. Over the year to then, the number of weekly flights in Europe reached around 9% below 2019, marking a clear improvement compared to 2022.

The chart below illustrates the average weekly flights across Europe based on data from Eurocontrol. As can be seen, the trend is roughly similar to last year, but at a level that is around 6-8% higher. Especially in the off-season, an improvement can be seen in 2023, with flights in February up to 30% above 2022, while the gap also narrowed with 2019 by the end of September and early October.

On closer inspection however, there is a great disparity between the various airlines in Europe and their contribution to the recovery. Analyzing the main airlines in the market, it becomes clear which ones lead the way and which are lagging.

The European recovery gathered pace in September and October.

© Dion Zumbrink

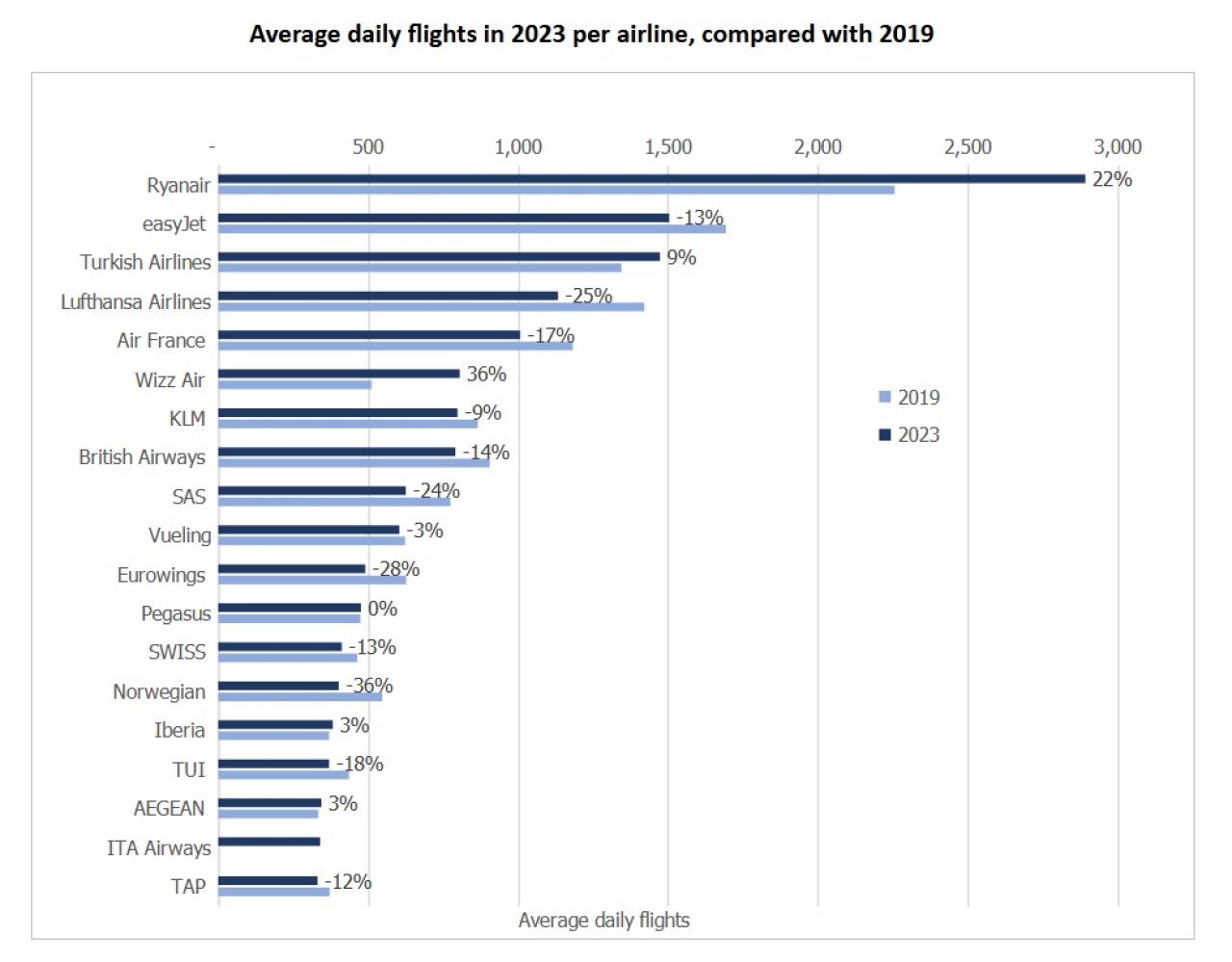

The second chart depicts average flights per day as registered by Eurocontrol. Just a handful of airlines are ahead of their 2019 level, with Ryanair easily in front in terms of total flights per day at close to 3,000. The carrier has widened the gap versus 2019 by an impressive 22%, while the next largest airline, easyjet, still lagging by 13% on its 2019 level.

Ryanair now operates almost twice as many flights in Europe as any other airline.

Other gainers were Turkish Airlines (+9%), Wizz Air (+36%), and, to a lesser extent, Iberia and Aegean (both +3%). Among the traditional full-service carriers, Lufthansa is the furthest away from a recovery, operating at 25% below its pre-pandemic level. While it had to give up the third spot to Turkish Airlines, it remained the largest of its Western European peers. Air France and British Airways are operating flights at 17% and 14% below 2019 respectively, with KLM doing a bit better, now 9% down on 2019.

Ryanair’s Post-pandemic Success

Ryanair has used the pandemic to its advantage. Due to its prior healthy cash position, back in September 2021, the airline was able to commit to large aircraft orders and plans for new bases in the upcoming five years until 2026.

A major factor in its success has been the B737 MAX with 197 seats and 16% more efficient fuel burn than its predecessor the B737 Next Gen. By July this year, the airline operated 124 B737 MAXs (re-branded by the airline as the ´gamechanger´ due to the start-up issues with the aircraft type). This brought the total fleet in use for the past summer to 565 aircraft.

Ryanair has moved far ahead of its rivals in building its share of the market.

© Dion Zumbrink

Ryanair still has over 400 aircraft orders outstanding before 2034. Future continued efficiency gains appear almost guaranteed with 300 B737 MAX 10 aircraft on order, which have 21% more seats and a 20% fuel efficiency gain over the B737 Next Gen. The fuel cost and other typical airline costs per seat will therefore decrease further.

The network for winter 2023/2024 was slightly reduced due to aircraft delivery issues by Boeing. Ryanair expected to receive 27 aircraft in the final quarter of the year, but due to production delays, only 14 aircraft are now expected. Before summer next year, the airline should, however, take delivery of 57 aircraft.

Pandemic Cuts Extract a Toll

Ryanair is also benefiting from the capacity constraints at other airlines, which struggle to ramp up as quickly post-Covid after having taken more drastic measures in reducing fleet and staff numbers during the pandemic.

Therefore, despite all the new capacity added, the airline has also been able to maintain its exceptionally high load factor of 96% during the summer and use the new aircraft straight away. In summer 2023, with the continuous delivery of new aircraft, Ryanair operated 190 new routes and continues to establish new bases, most recently in Belfast, Lanzarote, Copenhagen, and Tenerife.

The focus of the airline’s growth has been in Italy, where it operated over 50% more seats than in 2019, as well as France, Poland, and Greece which saw just under 50% additional seats. Italy is now the largest market for the airline, followed by Spain, the UK, and Ireland which saw growth of 18%, 15%, and 25% respectively. The only country which has significantly dropped was Germany, where the airline offered 26% fewer seats than four years ago.